The trend of consciousness and minimalism is influencing our daily lives. And personal budgeting is not an exclusion here.

Today, people understand the importance of proper personal finance management, and the demand for personal finance apps is growing.

The global personal finance app market is projected to reach US$406.5 billion by 2029. A survey by S&P Global Market Intelligence found that in the U.S., ~one-third of Americans use three or more finance apps.

Put together, these trends show one thing: personal finance app development is a smart business opportunity worth exploring.

But how to make it right to the users' hearts and stand out in the harsh competition of personal finance management apps?

I’m Yan Likarenko, a product manager at Uptech. In this article, I’ll break down the practical insights I’ve gathered from real projects to help you find a more detailed answer on how to build a finance app people will actually want to use.

So let’s get started!

The Core Foundations of Personal Finance App Development

All successful personal finance apps solve one fundamental job: they help users understand and manage their money across the full financial cycle. That’s the core value proposition — everything else is an enhancement on top of it.

In personal finance app development, your primary focus should always be on giving users clarity and control over their finances. And that starts with two key capabilities:

- Accurate tracking of income and expenses

- Clear, periodic analytics that help users see the bigger picture

These features form the minimum viable foundation for creating a finance app. Without them, even the most sophisticated features won’t matter, because users can’t trust the app as their single source of truth.

From there, you can extend functionality depending on your positioning and target segment. For example:

- Bank and payment integrations for automated data collection and a seamless money-management flow

- Gamification and goal-setting to motivate saving and reinforce healthy financial habits

- Smart notifications that surface unusual spending, upcoming bills, or savings opportunities

Think of these additions as ways to differentiate your product and increase long-term retention, but never at the expense of the core experience: clear, reliable financial visibility.

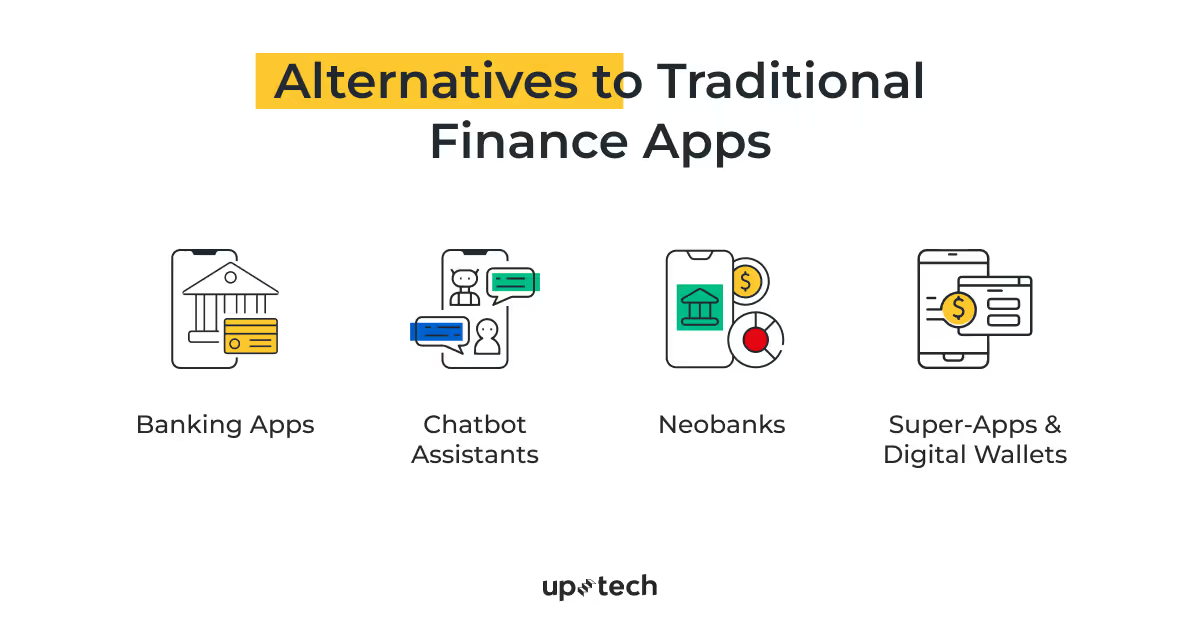

Alternative Types of Personal Finance Apps

When creating a personal finance app, you must assess not only your direct competitors but also those less obvious ones. Users increasingly get financial-management features from other, less obvious sources, and these “non-traditional” competitors can have a major influence on user expectations, product adoption, and retention.

Below are categories worth a deeper look when determining how to create a budget app that meets modern user expectations.

Chatbot assistants

Interestingly, the first competitor to keep in mind is not even an app. These chatbots are either integrated into banking or a messaging platform. Despite their lightweight nature, they are becoming serious alternatives to personal financial management apps because they remove two major adoption barriers: app fatigue and learning curve complexity. They help to manage the finances, assist with planning options, and even give individual advice.

Example: Plum.

Competitive advantages of financial chatbot assistants

- Frictionless onboarding: no full app download required

- High engagement: messages feel natural, not like “using a tool”

- Micro-interactions: users manage finances in small steps, embedded in daily chat flows

- Lower cognitive load: no dashboards, charts, or complex UIs to navigate

- Strong personalization: chatbot feels like a “financial buddy”

Weaknesses of financial chatbot assistants

- Limited visualization (charts, analytics, trends)

- Harder to manage complex financial structures (multiple accounts, assets, and so on)

- User trust relies on how well the bot’s logic is designed

- Can feel too “narrow” for users

Modern chatbot assistants can perform many of the same functions as classic personal finance apps, but with a simpler UX. For many users, especially younger or budget-casual audiences, conversational interfaces feel more accessible.

Banking apps

Strangely enough, banking apps are entering the niche of personal finance management apps. By integrating the features of financial analytics and savings achievements, they become a formidable competitor that provides banking and finance management features in one place.

Examples: Alliant Mobile Banking.

Competitive advantages of banking apps

- Single ecosystem: “one app for banking + personal financial management”

- High trust: banks are still perceived as more secure than independent personal finance management apps

- Native access to financial data: fewer syncing errors

- Instant money movement: easier to execute savings plans

- Built-in compliance/security

Weaknesses of banking apps

- Features often feel basic or generic compared to dedicated personal finance apps

- Limited personalization: analytics can feel “one-size-fits-all”

- Poor UX in some legacy banks

Want to learn how to integrate ChatGPT into your financial product? Check our article.

Neobanks

While traditional banks are slowly adopting personal finance features, neobanks are already operating as full-fledged personal finance management tools.

They offer much richer analytics, instant categorization, and AI-powered insights, often outperforming dedicated budgeting apps.

Examples: Monzo, Revolut, Chime

Competitive advantages of neobanks

- Built-in spending analytics and instant categorization

- Weekly or biweekly new feature releases

- Seamless international payments and currency transparency

- Strong mobile-first UX

- Real-time push notifications for every transaction

- Growing ecosystem of add-ons (subscriptions tracking, shared pots, savings vaults)

Weaknesses of neobanks

- Limited long-term financial planning tools

- Mostly focused on daily spending, not the full financial lifecycle

- No deep investment tracking (unless partnered with brokers)

- May lack robust budgeting frameworks (zero-based, envelope, etc.)

Neobanks directly compete with budget apps, not because users seek them out, but because users already manage money there without friction.

Super-apps & digital wallets

A growing share of users manage their day-to-day finances inside apps that were never designed as full-scale budgeting tools, but have become good enough for everyday money visibility. These apps solve the “quick financial check” problem far better than most personal finance apps, and this alone pulls users away.

Examples: PayPal, Venmo, Cash App

Competitive advantages

- Extremely high engagement: users open these apps multiple times a week

- Instant visibility into spending, subscriptions, and payments

- Built-in identity verification and payment rails

- One-tap adoption: no need to download an additional app

- Deep contextual data (purchases, merchants, devices)

Weaknesses

- Limited budgeting method support

- No advanced analytics or customizable dashboards

- Mostly focused on transactional visibility, not planning

- Hard to integrate large financial portfolios or assets

Users often feel these apps provide “enough insight,” reducing the motivation to download yet another finance tracker.

Top Personal Finance Apps on the Market

The market of personal finance apps continues to change. Here are several apps that are currently active, relevant, and shaping user expectations in 2025-2026.

Each comes with a unique positioning and set of strengths.

You Need a Budget (YNAB)

YNAB remains a standout for users who want hands-on control of their budgeting. It uses a zero-based budgeting method, so every dollar is assigned a role.

Perks:

- Ideal for disciplined budgeters who want to manage ahead of time rather than react.

- Strong community and methodology backing make it more than just an app.

PocketGuard

PocketGuard is well-positioned for users who want automated clarity on how much they can safely spend after bills and savings.

Perks:

- Real-time “safe to spend” calculation gives immediate value.

- Good entry-level free tier, with premium functionality.

EveryDollar

EveryDollar continues to serve the beginner and simplicity-oriented segment. It focuses on minimal fuss budgeting — especially the zero-based budget concept — with less complexity.

Perks:

- Quick to adopt, easy to use.

- Good fit for newcomers to budgeting apps

Goodbudget

Goodbudget operates on the envelope budgeting philosophy (for example, allocating money into “envelopes” for spending categories). This appeals to users who prefer analog budgeting methods translated into a digital format.

Perks:

- Digital version of a proven budgeting discipline.

- Clear visual categorization and spending control.

Simplifi by Quicken

Simplifi is emerging as a strong contender for users wanting all-around budgeting plus future cash flow projections.

Perks:

- Combines ease of use with more visually rich analytics.

- Bridges the gap between beginner tools and full-blown financial software.

4 Must-Haves When Building a Personal Finance App

Making a personal financial management app requires an individual approach, including in-depth business, user, and tech research.

With so many personal finance apps on the market, users have grown accustomed to polished, high-quality experiences. And they won’t settle for anything less.

To avoid disappointing them, here are some must-haves for your personal app’s service that I've learned from my own experience.

Visualization matters

Strong data visualization is what turns a personal finance app from “nice-to-have” into “I use this every day.” Anyone researching how to create a budget app quickly discovers that visualization is one of the most influential drivers of user retention.

When users open the dashboard, they should instantly understand where their money is going — no digging, no mental gymnastics. Clear spending breakdowns by category, merchant, or tag give them that quick snapshot.

Monthly cash-flow charts help them see the bigger picture, while trend lines show whether their income is quietly slipping below their expenses (or, ideally, the other way around).

A great personal finance app doesn’t just show the past, but hints at the future. Forecasts like projected balances or upcoming bills help users plan ahead instead of reacting too late. Even something as simple as color-coding can guide their attention: a subtle alert for overspending, or a gentle highlight when something looks unusual.

Good visualization removes friction, speeds up decision-making, and makes the whole experience feel smarter and more intuitive.

Security is a top priority

Giving up a part of your privacy to gain greater benefits has become a common practice in the modern, tech-driven world. However, things tend to get very sensitive when it comes to health or money. Solid data protection systems are paramount when creating a finance app.

A personal finance app must therefore not only be secure but also feel secure at every step of the user journey.

Instruments that you can use for higher fintech security are:

- Two-factor authentication (2FA)

- End-to-end encryption

- Instant notifications or alerts in case of unusual activity in the app

- A unique encryption key for every user

- Secure KYC process ( a multi-step process of users’ identity verification)

Here's our guide to fintech security best practices with a free security checklist. Check it out to ensure 100% protection for your app.

Intuitiveness is a standard

In such a complicated topic as finances, there is nothing more precious than ease. To bring real value to users, you need to make sure that completing a goal is no harder than switching on the TV or airing the room.

To reach ease and intuitiveness in your app’s flow, you should work hard on your UX. Or hire a team of UX designers who can do an excellent job for you.

Intuitive apps remove unnecessary mental effort by providing:

- Clean information hierarchy

- Clear terminology (no jargon unless you explain it)

- Simple categories and labels

- Predictable screen layouts

- Error-free automation (automatic categorization, smart defaults)

The rule is simple: If users have to think too much, the UX is failing.

Uptech’s protip: To make your UX effortless for users, you should know their pains and needs very well. Moreover, you should understand how your users live, how they spend their days, and when they go to sleep (well, maybe this one is too much). My point is: to make your app part of users’ lives, explore their lives first.

To learn more UX design tips for fintech apps, please check our blog post How to build a UX fintech design with a human face?

Keep up with the new reality

Make sure your personal finance app provides as many opportunities to your audience as reality requires. For example, many users expect at least basic support for popular coins like Bitcoin and Ethereum, along with digital wallet connections and simple value tracking. Even light crypto investors want these assets reflected in their overall financial picture.

Users no longer live in a single financial system. They mix:

- Traditional banks

- Neobanks

- Crypto wallets

- BNPL tools

- Digital payment apps

- Investments

- Savings platforms

A finance app that only tracks standard bank accounts feels outdated. A finance app that embraces modern financial behavior feels relevant, competitive, and future-proof.

Profound Discovery Is a Key to a Successful Personal Finance App Development

A strong discovery phase is the foundation of any successful personal finance app development process. Personal finance apps, in particular, require a deep understanding of user behavior, business constraints, and technical feasibility. Without this groundwork, even the best idea can fail to find traction.

Discovery is the stage where the team researches, validates, and clarifies the problem space. Its goal is simple: reduce uncertainty before development begins.

At Uptech, a discovery phase for personal finance products typically includes three core research tracks.

User research

Personal finance is emotional, private, and often stressful, which makes user research essential.

During this stage, our team learns:

- Users’ financial habits and daily routines

- Pain points and frustrations

- Motivations, fears, and decision-making patterns

- Tone of voice and communication expectations

This helps us shape a product that fits naturally into users’ lives instead of forcing new behaviors.

Tech research

Here, our experts explore the technical possibilities and limitations that will shape the solution:

- Which APIs and bank integrations are the best fit?

- What are the performance, security, and data-processing requirements?

- Which architectural decisions will ensure scalability and compliance?

This step prevents technical surprises later in the project.

Business research

The business research stage is necessary to assess all the business restrictions that would influence the development process. Typically, this includes:

- Stakeholder interview

- Problem statement

- Competitors research

- Business Model Canvas

- CJM (Customer Journey Map).

Apart from that, the discovery phase also includes making assumptions and validating the ideas.

Read more about the value of the discovery stage for your fintech business in our article Building a fintech app that stands the competition.

Must-Have Features to Make a Budget App

Once you’re done with the research and testing, you can start building your personal finance app. At this stage, you should have a list of must-have features figured out.

Here are the ones that you cannot miss.

Authorization and personal account

Make the process of authentication and onboarding as fast and easy as you can. Yet, keep in mind that it should be secure, as you are dealing with large amounts of personal information.

The user’s profile is necessary to allow users to keep all their personal information and be able to edit it at any time.

Income/expense tracking

Let users control transactions, get quick access to them, and use filtering to view data for a specific period.

Categorization

Allows users to categorize their expenses for clearer budgeting and management.

Notifications

Notify users of upcoming payments or rising expenses. Besides that, you can add additional functionalities to your personal finance app.

Financial goal setting

Allow users to set their financial goals, whether big or small. For example, saving up $200 weekly or working out a new financial habit.

Integration with other financial accounts/payment systems

Link your personal financial app to other financial services to streamline and synchronize financial services for users.

📲 Every fintech app needs to be fast, secure, reliable, and user-friendly. The Uptech team is here to help you develop one. Check out what financial software development services we offer.

Nice-to-have features

Once the core functionality is in place, you can add features that elevate the user experience and make your personal finance app stand out in a crowded market. These additions aren’t mandatory, but they can significantly boost engagement, retention, and perceived value.

Gamification: Add gamification to make your personal finances more engaging and fun. You could implement challenges, quests, or other game-like elements that encourage users to save more, spend less, or achieve specific financial goals.

Personalized financial advice: People like personalization. Especially when it helps them save money. Implementing a feature that provides personalized financial advice based on a user's unique situation could be a great idea.

Social responsibility score: The app could track the carbon footprint of purchases, or identify companies with poor labor practices and suggest more socially responsible alternatives.

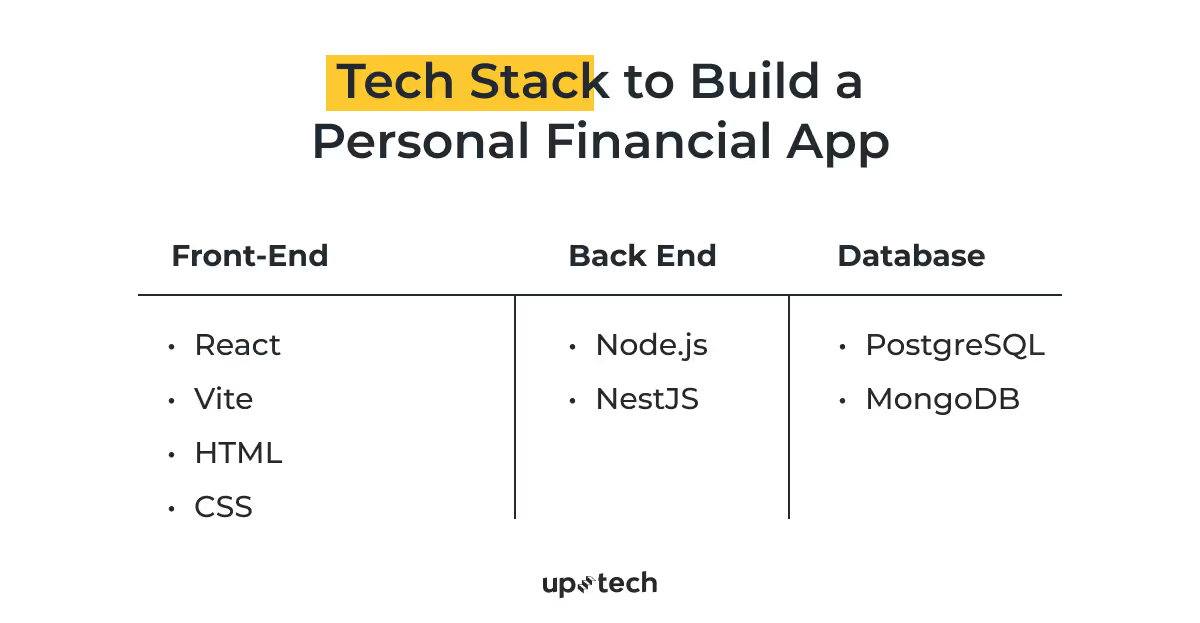

Tech Stack and APIs to Build a Personal Financial App

Once you have a list of functionalities for your budget-tracking app in your hands, select a list of instruments and technologies that you will use to develop the personal finance app. These can be libraries, programming languages, frameworks, etc.

Typically, the list of tech stack to build a finance app would include:

APIs

The list of APIs to build your personal finance app will depend on the feature scope, target markets, and the regulatory landscape of the bank you are partnering with.

In most cases, your app will need secure access to users’ financial data — transactions, balances, accounts, identity information — to generate analytics and insights.

For this, Plaid is one of the most popular and developer-friendly options. But Plaid is only one part of the puzzle.

Depending on your product’s functionality, you may also consider:

- Open banking: allows secure access to account data and payment initiation with explicit user consent. Ideal if you’re targeting EU/UK markets.

- Payment APIs (Stripe, PayPal, Wise, Cash App): useful if your app supports P2P transfers, bill payments, or automated savings rules triggered by user actions.

- Identity and compliance APIs (Persona, Alloy, Veriff): essential when you need KYC/AML verification, especially for apps that move money, offer financial advice, or connect multiple financial institutions.

- Investment and crypto APIs (Alpaca, Binance, Coinbase): required if you're integrating asset tracking, portfolio analytics, or crypto-wallet visibility.

- Notifications and messaging APIs (Twilio, Firebase): necessary for smart alerts, suspicious activity notifications, and authentication flows.

Cost of Building a Personal Finance App in 2026

The cost of the personal finance app development depends on a number of factors, like:

- Complexity of features

- Model of partnership with the team

- Hourly rate of the developers

But let’s imagine you are building a classic personal app.

Let’s take into account the average features for such an app, the cost breakdown will look the following way:

Uptech’s Expertise in Fintech App Development

With 10 years of building digital products, fintech app development has become one of Uptech’s strongest and most established domains. Over the past decade, we’ve helped both startups and mature financial companies turn complex ideas into intuitive, secure, and scalable financial products.

One example is a Green Investment App, where we led a full discovery phase to uncover users’ needs, pains, and decision patterns. Through interviews, usability tests, and hypothesis validation, we shaped a solution that fit naturally into users’ financial routines and proved its value in real-world use.

We also provide deep technical expertise — something we demonstrated in our long-term partnership with Aspiration, a financial app that helps users manage budgets while supporting socially responsible spending. Aspiration needed a more reliable and high-performing mobile experience, available to users 24/7. Our team migrated their iOS app from Objective-C to Swift, improving stability, performance, and scalability.

Today, the Aspiration app we developed is used by over 70% of their customers, holds a 4.9+ App Store rating, and supports 40,000 monthly active users — a testament to both technical execution and product-first thinking.

At the core of our fintech work is the Product Hypothesis–based approach, which ensures every feature is grounded in real user behavior, tested early, and refined continuously. This helps us build products that aren’t just functional, but genuinely empowering for the people who use them.

Conclusion

Building a personal finance app has all the ingredients to become a lucrative business opportunity. But the bar is high: users demand flawless UX, strong security, and real value from day one — and competition in the fintech space is only growing.

A thorough discovery phase and deep exploration of user needs are what turn a good idea into a product users genuinely rely on.

At Uptech, we’ve spent years building fintech and personal finance apps grounded in real research and real user behavior. We validate ideas early, test with users, design intuitive flows, and build reliable, scalable solutions — all with a clear focus on product–market fit.

Have a promising personal finance app idea but lack the technical expertise to bring it to life?

Partner with Uptech to confidently delegate the tech side and focus on what matters most: your vision.

Contact us, and let’s discuss how we can build your product together.