Fraud has gone not only digital, but also AI-driven. As threats grow more sophisticated, AI for fraud detection becomes essential.

Businesses are up to a new riddle — how to battle fraudsters with artificial intelligence up their sleeve.. This AI superpower already drives big losses, and it is predicted to take even more.

What exactly am I talking about?

According to Juniper Research, online payment fraud losses will exceed $343 billion globally between 2023 and 2027.

However, it’s not only about money. When businesses face fraud challenges and fail to beat them, they also lose:

- Reputation

- Operational efficiency

- Time (and sanity)

- And last, but certainly not least, market competitiveness

The good news? This isn’t AI fraud vs. businesses — it’s AI fraud vs. AI fraud detection.

Artificial intelligence, in this case, is neither a bad guy nor a good guy. It’s just a tool that both of them can use. Of course, to outsmart fraudsters, you need to be more strategic about AI fraud detection solutions.

My name is Oleh Komenchuk, I’m an ML lead at Uptech. I’m here to guide you through any AI fraud detection complexities and help you implement AI in a way that would secure your business from fraudsters.

Let’s begin!

What is AI in Fraud Detection?

Let’s talk about the definition of AI fraud detection first. What exactly does it mean?

In simple terms, AI in fraud detection uses machine learning (ML) and advanced analytics to automatically identify and prevent fraud in payments, identity verification, or online transactions.

How is this different from old-school, rule-based systems? Basically, they’re like fixed checklists — mostly useful, but fraudsters can game them. AI, on the other hand, is a slick detective who:

- Learns from historical data and adapts to new fraud tactics in real-time

- Can handle insane volumes of data

AI doesn't just fight fraud, but also outsmarts most scam schemes. And the best part? It doesn’t get tired, never takes days off, and only gets better with time. That’s definitely a partner you need by your side in modern digital dynamics.

Traditional fraud detection methods and their limitations

As mentioned earlier, before AI-driven solutions existed, fraud detection primarily relied on two methods: rule-based systems and manual reviews. These approaches were effective in simpler times, but they now struggle to keep pace with the increasingly advanced tactics of online fraud.

Today, these traditional methods often create as many problems as they solve, especially with the complexity of modern digital user behavior. In some cases, 95% of alerts generated by rule-based systems end up being false positives, leading to unnecessary investigations and customer dissatisfaction

To fully grasp their limitations, it’s important to go through their drawbacks in detail.

AI isn’t just being called the future of fraud detection because it’s the latest trend. When we see the gaps in older systems and recognize how AI steps in to fill them, it becomes clear why artificial intelligence fraud detection is now at the forefront of advancing fraud detection.

Rule-based fraud detection

Rule-based fraud detection identifies fraudulent activities with predefined rules or conditions for transactions, user behaviors, or system events.

So, practically, it works like this:

- Team sets the rules (example: “Block if payment is more than $5,000 from a new account”)

- A rule-based fraud detection system checks every transaction

- It flags or blocks a transaction if a rule is broken

Sounds not bad at all, right? However, in real life, it’s not really that practical. Rule-based fraud detection systems:

- Сan't tell good weird from bad weird. That time the user splurged on a fancy anniversary gift? Blocked. Vacation purchases abroad? Account frozen. Meanwhile, actual fraudsters have figured out how to fly under the radar.

- Waste real money. On average, these systems reject 1 in every 10 legitimate transactions. Imagine turning away 10% of your paying customers at the door. That's basically what's happening.

- Create more work for everyone. Your fraud team spends all day reviewing false alarms while real threats slip through. Your customers get frustrated dealing with locked accounts. Nobody wins.

Overall, the biggest problem of this approach to fraud detection is static logic in a very dynamic user behavior space. Fraud patterns advance, rule-based systems don’t. Of course, fraudsters will take their chance to study these systems, find gaps, and use them to their advantage.

More to add, they’re also narrow and binary. A transaction either matches a rule or it doesn’t. There’s no nuance. No context. No ability to detect patterns across multiple data points like user behavior over time, device fingerprinting, or network anomalies.

Manual reviews

Besides rule-based fraud detection systems, many companies still use human teams to manually check suspicious transactions. Sure, humans have good judgment skills. The human mind has the ability to notice nuance and context more than any machine can do.

However, this old-school approach has some big problems.

- Fraud moves fast, humans don’t. A scammer can drain an account in seconds, but by the time a person finishes reviewing the case (hours or even days later), the money’s long gone. Imagine someone hijacking your account and emptying it before fraud teams even start looking into it.

- It just doesn’t scale. During busy times (like holiday shopping sprees), fraud spikes, but you can’t just hire an army of reviewers overnight. Manual checks buckle under the pressure.

- People get tired, AI doesn’t. When analysts have to review hundreds of transactions a day, even the best ones miss things. Meanwhile, AI spots sneaky patterns humans overlook.

Don’t get me wrong, these old methods worked okay in their time. But fraud today is faster, smarter, and way more aggressive. Relying on slow, error-prone manual reviews is like bringing a flip phone to a hacker convention.

AI-Powered Fraud Detection: How It Works

Now that you understand traditional fraud detection methods, let’s explore fraud detection with AI implementation.

Why are these systems better? How do they actually work? Time to pull back the curtain and examine the mechanics behind them.

AI-powered fraud detection is a complex system of advanced technologies working together to identify, analyze, and prevent fraud with great precision.

Five core components make it possible:

- Machine learning models. They detect patterns, classify transactions, and adapt to new fraud tactics.

- Natural language processing (NLP). It analyzes text (emails, claims, chats) for scams or social engineering.

- Anomaly detection systems. They flag outliers in real-time, like unusual logins or payments.

- Predictive analytics. It forecasts risks by combining historical data with real-time signals.

- Graph AI and network analysis. They uncover hidden connections like fraud rings or money laundering.

With all these smart technologies, AI creates a safety net that is both resistant and smart. It catches what rule-based systems miss, adapts to new scams as they appear, and even helps avoid annoying false alarms that block real customers.

Now, let's take a closer look at each of these pieces to see how they team up to stop fraudsters in their tracks.

Machine learning models — fraud detectors

When it comes to machine learning models, modern fraud detection systems usually employ two complementary types of machine learning — supervised and unsupervised. They work together like a detective duo. The first one memorizes known criminal cases, and the second one spots suspicious behavior in real-time.

Let’s break them down to understand their dynamic.

Supervised learning

Supervised learning models are trained on labeled datasets, which require human annotators to manually classify or tag the data — a crucial but often labor-intensive task. Each data point (transaction, email, login attempt, and so on) is labeled either fraudulent (fraud activity) or legitimate (normal activity).

The machine learning model studies thousands of examples of confirmed fraud, like stolen card transactions. Then, it analyzes features like transaction amounts, IP addresses, time stamps, and behavioral biometrics (typing speed, for example). And finally, with time, it builds a predictive model that flags new transactions matching these fraud patterns.

Once trained, supervised models catch fraud that follows established patterns. Unlike rule-based systems, AI considers context, so legitimate high-value transactions from a trusted user most likely won’t be flagged.

Unsupervised learning

Contrary to previous, unsupervised learning models don’t rely on pre-defined data. Instead, they analyze raw transaction logs, user behaviors, and network traffic to discover hidden patterns, anomalies, and unusual behaviors — data points that don’t fit normal patterns.

Unsupervised learning uses a couple of techniques like clustering, autoencoders, and isolation forests.

- Clustering algorithms group similar transactions together based on shared features, such as amount, location, device ID, frequency, or merchant type. They form clusters based on similarity and spot transactions that fall far from any cluster, outliers.

For example:

- Cluster A: Daily $5–$15 food purchases, same device, same location.

- Cluster B: Monthly $1,000–$2,000 rent or bill payments.

- Outlier: A $9,500 wire from a new device in another country.

If that outlier doesn’t fit any cluster, the transaction will be flagged for review.

- An autoencoder is like a super-observant assistant. You show it thousands of normal purchases, and it learns them so well it can recreate them perfectly. Then, when you give it a fraudulent transaction, it struggles to copy it accurately, and the "mistakes" it makes reveal the fraud. That mismatch sets off an alarm.

- Imagine playing Guess Who? with a machine. With the Isolation Forest algorithm, the algorithm asks random yes/no questions to narrow down transactions: "Is the amount under $100?", "Was it made in the user’s home country?" — until it quickly flags the suspicious activity.

Normal transactions follow a common path and take more steps to sort out. Suspicious ones get isolated quickly because they’re different. For example, a thief tries five $1 charges in a row on a stolen card. That’s not typical behavior, so the system spots it fast.

Fraud detection has come a long way: no more relying solely on rigid rules that fraudsters can easily outmaneuver. Thanks to machine learning, we now have systems that learn, adapt, and get smarter over time.

Natural language processing (NLP)

Natural language processing (NLP) helps AI systems read, interpret, and analyze language, whether it’s in emails, chat logs, transaction notes, or even voice recordings. But it doesn’t just process words..

Here’s how it works:

- It understands context, not just keywords, but the meaning behind them.

- It spots emotional triggers (like urgency or fear) that scammers often use.

- It detects anomalies, like sudden changes in writing style or mismatched details.

- It learns and adapts, getting better over time as it processes more data.

In short, NLP gives AI the ability to ‘read between the lines,’ making fraud detection faster, smarter, and far more effective.

How NLP helps prevent fraud detection

Text analysis for phishing and scam detection. NLP algorithms can scan emails, chat messages, and social media posts to detect phishing attempts and fraudulent schemes. It analyzes linguistic cues, such as threats or suspicious requests, and flags potential scams before they cause harm.

Sentiment and deception detection. Fraudsters often manipulate language to appear trustworthy. NLP models trained on large datasets can detect subtle signs of deception, such as overly formal or unnatural language or inconsistent narratives.

Identity verification and synthetic fraud prevention. The rise of deepfake audio and AI-generated text is already here. NLP can verify the authenticity of the sound and prevent synthetic identity fraud by detecting AI-generated content and analyzing voice biometrics.

Transaction monitoring and anomaly detection. NLP processes unstructured data like customer support chats or transaction notes to identify suspicious behavior. For example, unusual changes in customer writing style (indicating account takeover) or mismatched descriptions in financial documents.

To sum up its capabilities, NLP is transforming fraud detection from reactive to proactive and intelligent.

Anomaly detection systems

Anomaly detection refers to the process of identifying rare events, outliers, or suspicious patterns that significantly differ from normal behavior. In fraud detection, these anomalies could be:

- Unusual transaction amounts

- Irregular login locations

- Strange purchasing patterns

- Abnormal account behavior

AI-driven anomaly detection goes beyond static rules — it learns normal behavior patterns and flags anything that doesn’t fit.

How does it work in practice?

Imagine your typical morning routine: you check your bank account from your home WiFi at 7:30 AM using your phone. An anomaly detection system learns this pattern. Now consider these scenarios:

- A login attempt from China at 3 AM

- A $5,000 wire transfer to a new recipient

- Five failed password attempts in two minutes

The system would flag all these as potential red flags because they break your established patterns. But here's the clever part — it doesn't just look at one factor in isolation. It considers dozens of signals simultaneously:

- Device fingerprints — is this the same smartphone you always use?

- Behavioral biometrics — do you type at your usual speed?

- Network signals — is this coming from your typical location?

- Timing patterns — do you normally bank at this hour?

What makes modern anomaly detection particularly powerful is its ability to adapt. As users change their habits — maybe users start traveling internationally or buy a new laptop — the system quietly updates its understanding of “normal” for them. This prevents false alarms while maintaining strong security.

At the same time, it's constantly learning about new fraud patterns across the entire network. When it spots a new attack method targeting one customer, it can instantly protect all others from the same threat.

Predictive analytics

Predictive analytics powered by artificial intelligence gives organizations the ability to anticipate and prevent fraud before it occurs. AI systems transform fraud prevention from a game of catch-up to strategic defense with the help of historical patterns.

At its core, predictive fraud detection combines three powerful capabilities:

- Learning from the past. A confirmed fraud case becomes a lesson, helping the system recognize similar patterns in the future.

- Monitoring the present. It analyzes user behavior in real-time and spots deviations as they happen.

- Calculating risk. Advanced statistical models assign fraud probability scores to every transaction.

These systems don't just flag existing fraud patterns. They forecast where and how fraud is likely to occur next, quietly assessing dozens of factors. That moment when you make an online purchase? A sophisticated fraud check happens in the blink of an eye:

- Your personal patterns — do these match your usual spending locations, times, and amounts?

- Merchant reputation — has this seller been linked to recent fraud activity?

- Behavioral red flags — does this transaction fit known account takeover tactics?

All this analysis happens seamlessly while you wait for your payment confirmation.

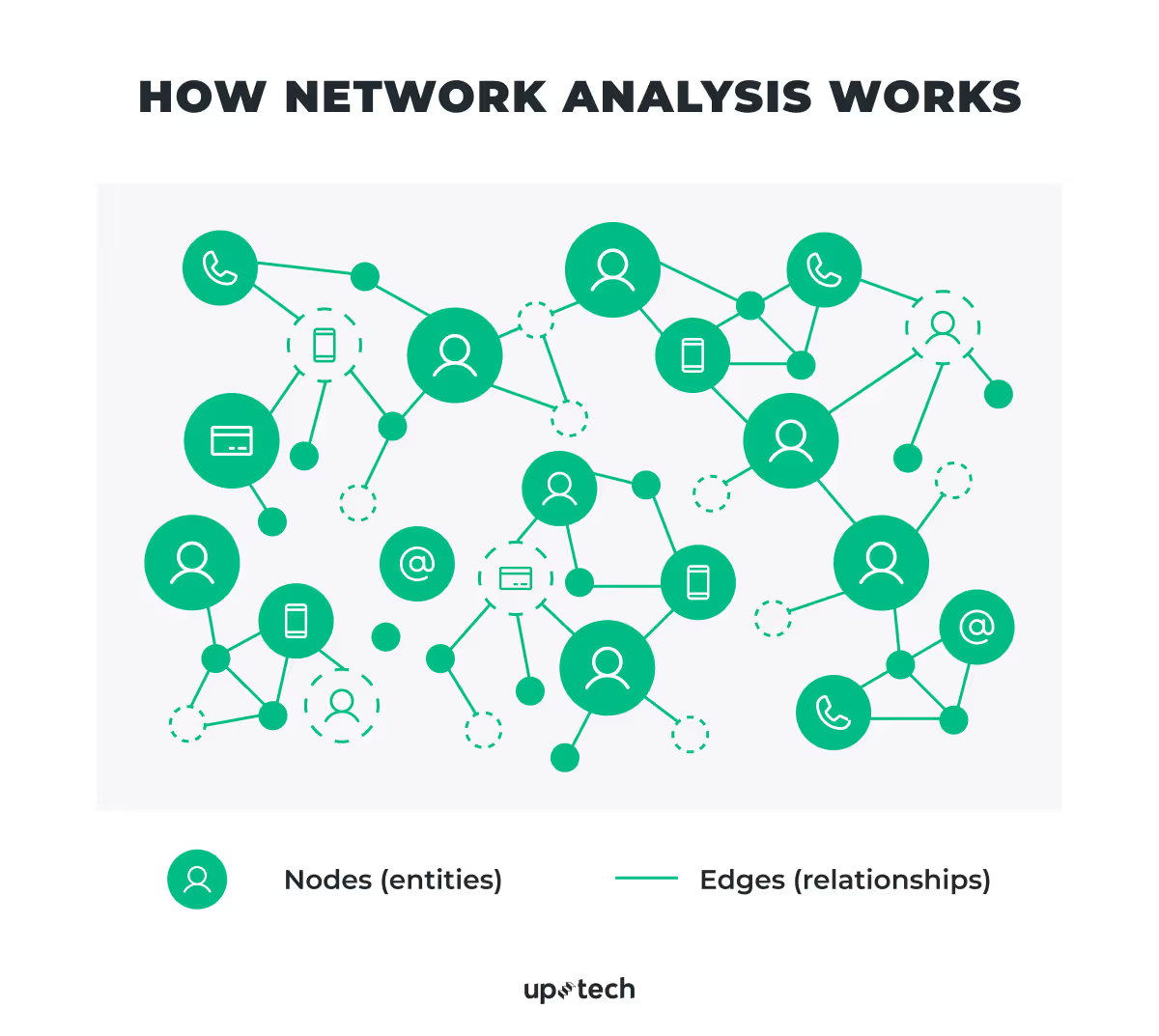

Graph AI and network analysis

Graph AI maps relationships between people, accounts, devices, and behaviors and turns raw data into a dynamic network (graph) of entities and their interactions.

Nodes represent entities like users, accounts, devices, email addresses, phone numbers, or IPs.

Edges represent relationships such as financial transactions, shared logins, geolocation proximity, device usage, or social connections.

Instead of asking, “Is this transaction fraudulent?”, Graph AI asks, “How is this transaction connected to a larger pattern of fraud?”

It creates a dynamic map of:

- Accounts linked by shared devices or IP addresses

- Payment flows between suspicious entities

- Clusters of fake identities created from stolen data

- Patterns of coordinated attacks across multiple targets

What Graph AI detects that traditional systems miss

Synthetic identity fraud rings. Fraudsters often create “synthetic” identities, a mix of real and fake data, to open fraudulent accounts. Individually, these accounts may look legitimate. But when viewed as a network, clear patterns emerge.

Graph AI detects:

- Clusters of accounts sharing device fingerprints, email patterns, bank credentials, or contact details

- “Star-shaped” networks, where one real identity is linked to multiple synthetic ones

- Coordinated account creation across platforms or financial institutions

Coordinated account takeover (ATO) attacks. Credential-stuffing and brute-force attacks are often tested across multiple accounts and platforms to find weak links. Graph AI uncovers the scale and coordination behind these intrusions.

Graph AI detects:

- Multiple failed logins from the same IP/device targeting a wide range of accounts

- Reuse of stolen credentials across different services

- Shared infrastructure (VPNs, proxies) linked to known attack campaigns

Collusion and insider fraud. When fraud involves insiders (employees or partners), it gets trickier. Insider actions may look legitimate on the surface, but Graph AI can reveal hidden connections and behavioral outliers.

Graph AI detects:

- Employees consistently approving questionable transactions tied to the same vendors or customers

- Overlap between internal users and flagged external entities (shared contact info, IPs, or device usage)

- Patterns of unusual data access or system behavior

Real-World Use Cases of AI in Fraud Detection

Let’s dive into three big areas where AI is making waves: financial fraud, sketchy online shopping schemes, and healthcare billing scams.

Financial services: AI for banking and payments fraud

Imagine a stolen credit card is used for a high-value purchase in a foreign country. Just a few years ago, the transaction might have slipped through unnoticed until the real cardholder reported fraud days later. Today, however, AI changes the game.

Banks now use machine learning to analyze hundreds of transaction details in real time, checking every purchase against a customer’s normal spending habits. If something looks suspicious, like a sudden splurge on a luxury item in a different time zone, the system can flag it and block the transaction before it even goes through.

Take HSBC, for example. They’ve implemented graph neural networks (GNNs) — the same AI tech I described earlier. It maps out financial connections like a detective piecing together clues. Their system sifts through over transactions every month and uncovers hidden money laundering patterns that even the sharpest human analysts might miss. And the results don’t lie: 60% fewer false alarms for customers, while catching more real financial crimes than ever.

E-commerce: AI in payment fraud and fake reviews

Online shopping should be fun, not a minefield of fake reviews and stolen credit cards. Ever seen those suspiciously perfect five-star reviews that all sound the same? AI spots them instantly by analyzing writing patterns, down to the way commas are used.

Amazon uses smart AI to keep its marketplace safe from scams. These systems constantly analyze how users behave, what they’ve bought before, and even the devices they use, to spot anything fishy. Say a brand-new account suddenly tries to buy five flat-screen TVs in an hour? Amazon’s AI will catch that red flag and block the transactions before any damage is done.

But it’s not just about payment fraud. Amazon’s AI tackles fake reviews, too. It scans for sketchy patterns, like copy-pasted phrases or a flood of five-star ratings at 3 AM, and weeds out the suspicious ones. That way, users get real feedback from actual customers.

Healthcare: insurance fraud and patient data protection

Healthcare fraud hurts more than just wallets. It puts patients at risk and breaks their trust in the system. Consider scenarios like billing for 24 hours of physical therapy in a single day or unauthorized access to patient records by hospital staff who have no treatment relationship with the patient. Such actions not only strain healthcare resources but also compromise patient safety and privacy.

One striking example is the $1.2 billion healthcare fraud case uncovered by the U.S. Department of Justice, where fraudulent billing schemes exploited vulnerable patients, including seniors and terminally ill people. Providers submitted false claims for unnecessary medical services, some of which were never even rendered. This case underscores how systemic fraud can drain billions from the healthcare system while endangering patient well-being.

Again, AI smart algorithms can spot suspicious patterns that humans might miss. These systems are trained to catch red flags like:

- Phantom billing (charging for services never rendered)

- Upcoding (billing for a more expensive procedure than was performed)

- Unusual access patterns to sensitive patient data

Benefits of AI in Fraud Prevention

Fraud is a huge risk for fintech, e-commerce, and banking, costing businesses millions. AI offers scalable and ultra-accurate protection. Here’s how:

Real-time monitoring. Old fraud detection methods are too slow. AI spots and flags fraud as it happens and cuts losses fast. For leaders, this means stronger security and less risk.

Handles growth effortlessly. More transactions = more fraud risks. Human teams can’t keep up, but AI scales easily, analyzing massive data without losing accuracy. For CEOs and CTOs, it’s a cost-effective, long-term shield.

Fewer false alarms. Legit transactions wrongly flagged as fraud frustrate customers and waste time. AI’s machine learning slashes false positives, improving customer experience and cutting unnecessary costs.

Adapts to new threats. Fraudsters keep changing tactics. AI learns continuously, spotting new patterns faster than old rule-based systems. For businesses, this means staying ahead of threats, not just reacting to them.

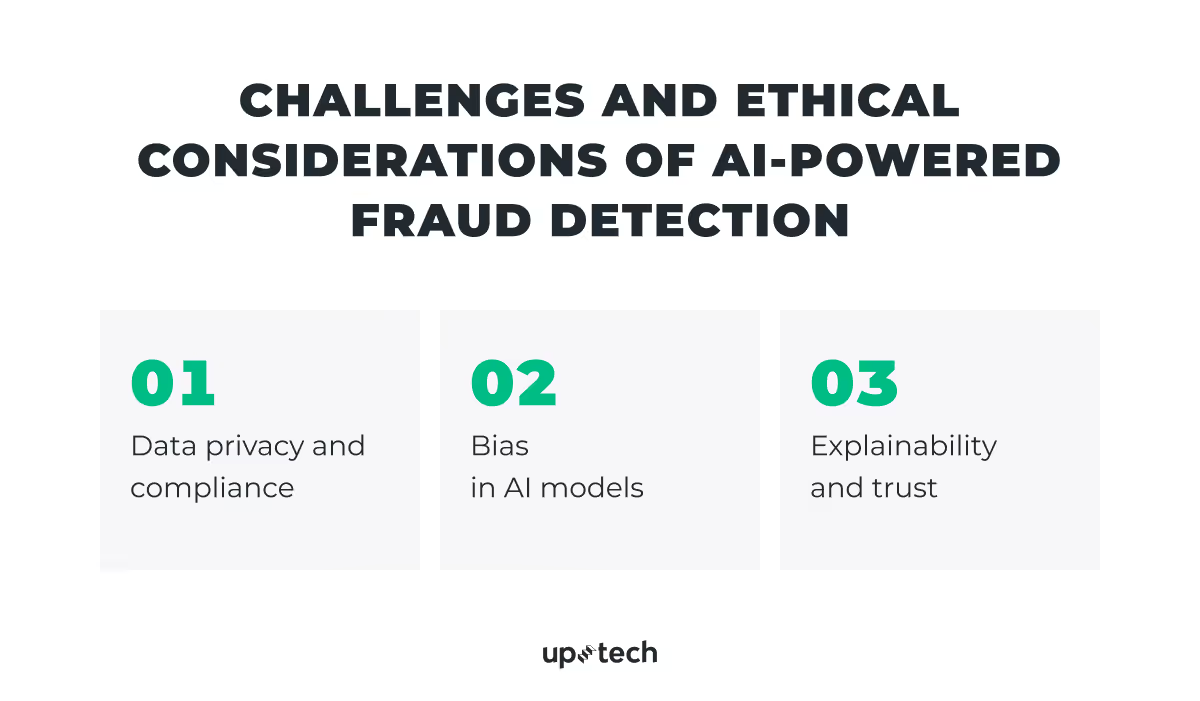

Challenges and Ethical Considerations

With great, helpful solutions come great challenges and responsibilities.

Using artificial intelligence for fraud detection raises important questions about ethics and legal compliance — things every business needs to think about before getting started.

Data privacy and compliance

AI systems, including AI-powered fraud detection systems, require a lot of data to train on. They also have access to internal sensitive data: payment histories, IP addresses, behavioral patterns, and even biometric identifiers. Without proper safeguards, there’s a high risk of violating data protection laws like GDPR (EU), CCPA (California), and others that govern how data is collected, processed, and stored. And, of course, drive big troubles upon your business.

To avoid trouble:

- Choose solutions that only collect and process the data that’s absolutely necessary for fraud detection.

- Mask personal identifiers to reduce the risk of exposure in case of a breach.

- Schedule periodic reviews of how data is collected and used to check alignment with regulatory requirements.

Bias in AI models

AI systems will be unbiased only if trained on unbiased data. In another case, if datasets contain any societal or institutional biases, AI may reflect them or even amplify those patterns. In fraud detection, an AI solution can disproportionately flag suspicious transactions from certain geographic locations or income groups. That is highly inappropriate and will damage your users’ trust and product reputation in the long run.

How to prevent it?

- Use data that represents various transaction types and user groups to reduce the risk of discriminatory behavior.

- Engage human fraud analysts to review automated decisions, especially high-impact scenarios.

- Use tools like IBM AI Fairness 360 or Microsoft Fairlearn that test and highlight bias in models before deployment.

Explainability and trust

It is hard for users to trust and understand AI interactions completely. This lack of transparency in AI decision-making is a big issue when legitimate users are mistakenly flagged, and there's no clear explanation as to why.

To deal with this, try to:

- Always provide users with a clear reason why a transaction was declined or flagged.

- Incorporate explainable AI to provide insights into why a decision was made.

- Maintain internal documentation that explains how the AI system works.

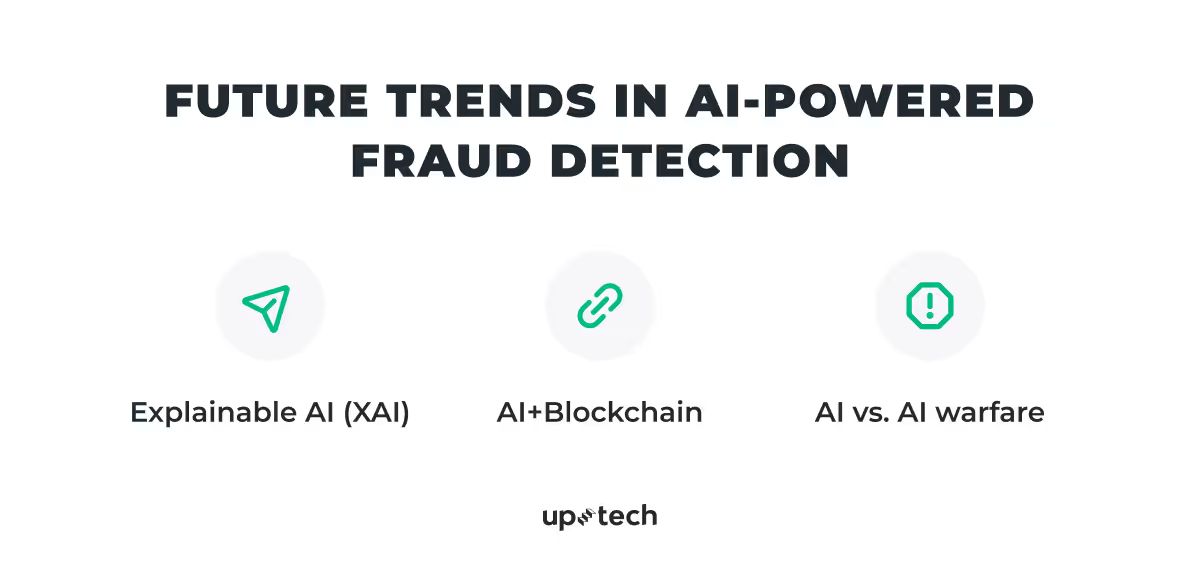

Future Trends in AI for Fraud Detection

Fraudsters are getting more creative with AI implementations. Every AI advancement cuts both ways — it supports sophisticated scams, but also is the best tool to counter them.

For businesses, it means that every new fraud tactic should be met with a smarter detection approach. Fortunately, AI fraud detection evolves fast enough to provide many great options for those who need them.

Let’s break down future AI fraud detection trends, why they matter, and what they mean for security.

Explainable AI (XAI) — no more guesswork for the users

Most AI fraud detection systems work like a strict but silent security guard. They shut down suspicious activity, but usually won’t explain hy they did so. Sometimes it breaks users’ trust and makes them frustrated.

Explainable AI (XAI) doesn’t just flag fraud but provides a detailed breakdown of its decision-making process.

For example, instead of a vague alert, XAI explains:

“The login attempt is suspicious because the IP address is from a country the account has never accessed before”.

XAI builds trust through ‘such fraud decision explainers’ for end-users and makes life easier for fraud analysts since they get AI reasoning for flagging suspicious activities. Less black-box mystery, more "Here’s why this looks sketchy." Result? Higher trust, faster decisions, and fewer false alarms.

AI+Blockchain — the ultimate fraud-proof tag team

Scammers often alter records to get what they want: fake invoices, duplicate transactions, and so on.

With traditional datasets, it’s possible to manipulate data with processing delays and modified transaction records, which makes it quite hard to trace fraud.

Fraud loves chaos. Blockchain loves order. If we combine AI’s pattern-spotting with blockchain’s immutable records, suddenly, every transaction has a verifiable trail.

- AI detects suspicious activities.

- Blockchain locks every transaction in an unchangeable ledger.

For example, the buyer pays, and the transaction is recorded on the blockchain. The supplier tries to resubmit the same invoice (hoping the buyer pays twice). AI flags the duplicate, and blockchain proves the original payment is already logged. The fraud fails instantly, no manual audit needed.

AI vs. AI warfare — the arms race nobody signed up for

Fraud has entered a digital era with a strong AI backbone, and scammers enjoy it to the fullest.

Machine learning algorithms help them in many ways: to mimic behavior, bypass traditional security measures, and even generate convincing deepfake audio to scam victims.

Two sides are locked in an endless battle:

Attackers (fraudsters, hackers, even state actors) use AI to:

- Automate attacks — deploy phishing scams or spam at unprecedented scale.

- Evade detection — mimic human behavior to bypass traditional security.

- Develop new exploits — use machine learning to find vulnerabilities faster than humans can patch them.

Defenders (businesses, cybersecurity firms, governments) counter with AI that:

- Predicts threats — spots subtle anomalies in real-time (like a login that almost matches a user’s habits).

- Adapts quickly — learns from each attack to strengthen defenses.

- Fights deception — detects deepfakes, synthetic identities, and AI-generated disinformation.

How Uptech Can Help You Fight Fraud Using AI?

Fraud is a growing threat across industries. Every year, businesses lose billions, and customer trust takes a hit. Old-school, rule-based systems can’t keep up as fraudsters get sneakier. This is where custom AI-powered fraud detection solutions make a critical difference.

At Uptech, we build custom AI fraud detection designed for your industry’s toughest challenges.

Banking and fintech solutions

Our AI models detect real-time payment fraud, identify synthetic identities, and uncover sophisticated money laundering schemes, all while reducing false positives that frustrate legitimate customers.

Healthcare protection systems

We help prevent fraudulent insurance claims before they're paid out and secure sensitive patient data with adaptive algorithms that learn new attack vectors as they emerge.

E-commerce defense platform

From fake review detection to chargeback prevention, our solutions automatically identify and block fraudulent activity while protecting genuine customer accounts from takeover attempts.

Insurance fraud detection

AI fraud detection solutions analyze claims to flag staged accidents, spot exaggerated injuries, and detect provider billing anomalies with unprecedented accuracy, and speed up legitimate claims processing.

Overall, we build custom AI systems that:

- Learn your specific risk patterns (so you block more fraud, fewer good users).

- Automate decisions in real time (no more backlog of manual reviews).

- Grow smarter with every attack (because fraud never stands still).

With AI that learns as fraud evolves, you’re not just reacting but preventing. Less loss, more trust, and peace of mind. Ready to outsmart fraudsters? Let’s build a solution that adapts as fast as they do. Contact us for a free consultation.

FAQ

How does Uptech use AI to prevent fraud in fintech products?

At Uptech, we build financial platforms with AI at their core, so their security gets smarter with every transaction. Our AI solutions don’t just react; they learn, predict, and adapt in real time to keep your business safe.

Here’s how we can help you fight fraud:

- We combine multiple machine learning models to catch both known fraud patterns and new, emerging threats and reduce false alarms by understanding real user behavior.

- We design systems that automatically adjust security levels based on real-time fraud trends, individual user habits, and the latest threat intelligence.

- We go beyond basic fraud detection with deepfake-proof identity checks (spotting AI-generated faces and fake documents), network analysis, and a transparent approach to AI creation and optimization.

However, every business is different, so we don’t believe in one-size-fits-all solutions. We take the time to understand your unique challenges and build a fraud prevention strategy that fits.

Want to see how we can protect your fintech product? Contact us for a free consultation. Let’s discuss your needs and find the best solution together.

What are the best fraud detection solutions for fintech/e-commerce?

The best solution depends on your business size, industry risks, and budget. Fintechs may prioritize collaborative networks or behavioral biometrics, while e-commerce brands often benefit from chargeback protection or device intelligence.

Fraud detection solutions for fintech

AI/ML-based fraud scoring reduces false positives in legitimate transactions while identifying complex fraud patterns like money laundering or synthetic identities.

Behavioral biometrics detects account takeovers by analyzing unique user interactions like typing rhythm or touchscreen gestures.

Real-time transaction monitoring identifies suspicious payment activity as it happens, preventing fraudulent transfers before completion.

Identity verification validates user identities through document checks and liveness detection to prevent fake account creation.

Anti-money laundering (AML) screening flags high-risk transactions and identifies sanctioned individuals or politically exposed persons.

API security and bot mitigation protects against automated attacks targeting financial APIs and login systems.

Blockchain analytics tracks cryptocurrency movements to detect illicit transactions and suspicious wallet activity.

Network link analysis uncovers organized fraud by mapping connections between accounts, devices, and transaction patterns.

Fraud detection solutions for e-commerce

Payment fraud prevention blocks unauthorized transactions while minimizing false declines that frustrate legitimate shoppers.

Device fingerprinting recognizes returning fraudsters even when they attempt to disguise their devices or locations.

Chargeback protection provides financial guarantees against fraudulent disputes, protecting revenue.

Account takeover prevention stops credential stuffing attacks that compromise customer accounts.

Promotion abuse detection identifies and blocks fraudulent use of discounts, coupons, or loyalty programs.

Return fraud prevention detects patterns of abusive return behavior like wardrobing or empty-box scams.

Guest checkout screening assesses risk for one-time purchasers who don't create accounts.

Bot mitigation prevents inventory hoarding by scalpers and automated checkout bots.

What are the main features of fraud detection software?

Here’s a breakdown of the main features that empower fraud detection software systems to detect anomalies, assess risk, and adapt to emerging threats:

- Real-time transaction monitoring — to analyze transactions (payments, logins, account changes) in milliseconds using rule-based engines and anomaly detection.

- Machine learning models (both supervised and unsupervised) — to detect known fraud patterns and emerging threats.

- Multi-factor risk scoring — to assign dynamic risk scores to each transaction based on device intelligence, biometric verification, and behavioral biometrics.

- Network and link analysis — to detect organized fraud rings through mapping relationships between entities (like shared devices, payment methods, or shipping addresses).

- Automated decisioning and case management — to provide fraud analysts with case prioritization, audit trails, and collaborative tools for investigations.