The boom in fintech funding saw huge amounts of money flowing into so-called neobanks, digital financial companies that offer banking services in the most innovative ways.

Many traditional banks are brick-and-mortar: The services cost more and engage customers less. This is where the need for neobanks arises. If you're wondering how to build a neobank – a digital-only bank that relies on modern technologies to deliver financial services, this guide will walk you through the key steps.

We at Uptech have helped develop several neobanks, including big names like GreenFi. We know first-hand how to start a neobank, what features to add to stand out from the crowd, and how to help you build a neobank that engages users. There's a lot to cover, so let's start!

What Is a Neobank and How Does It Work?

First things first, let's figure out what a neobank is, how it works, and name some good examples.

What is a neobank?

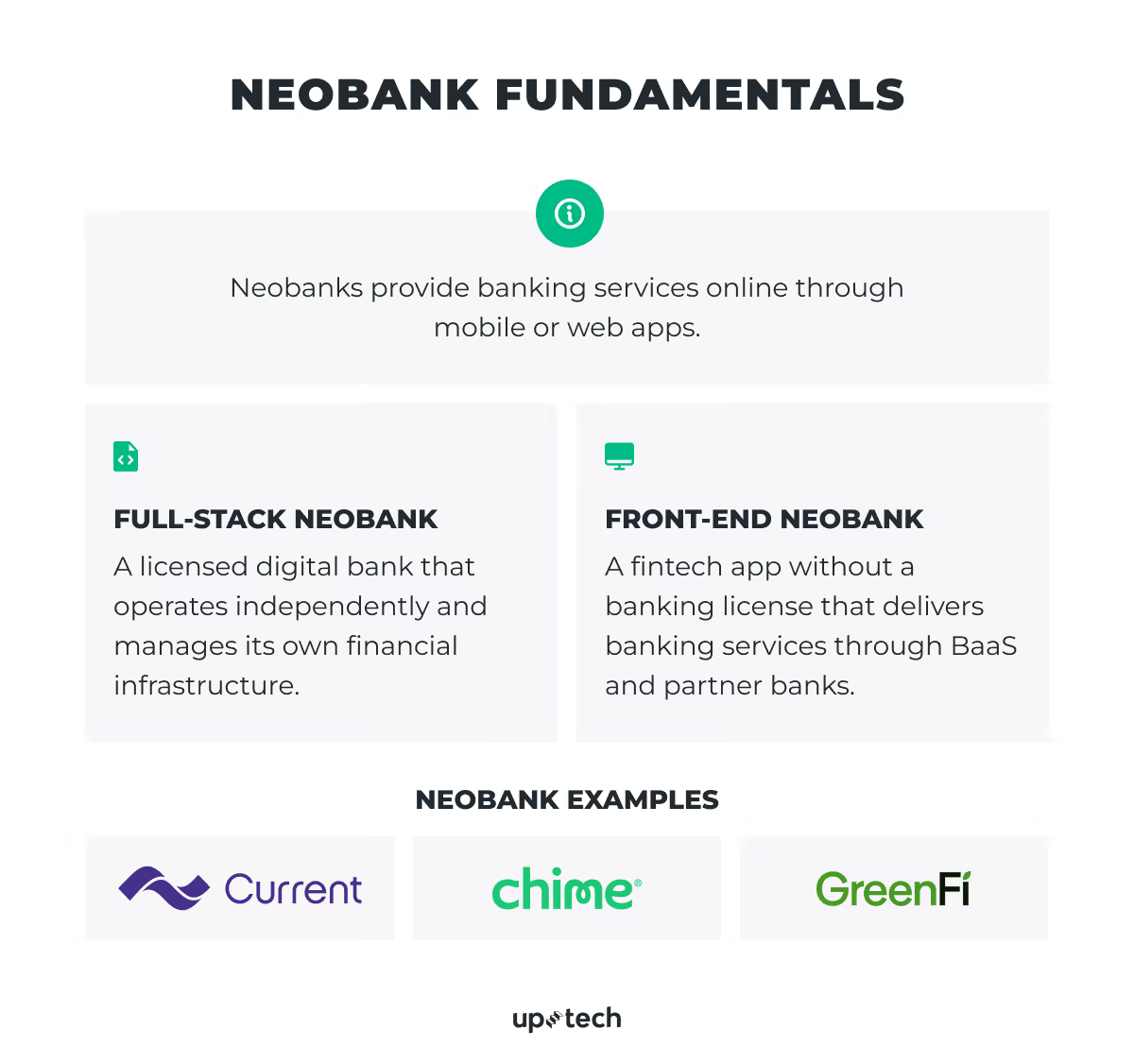

A neobank is a bank that has only an online presence with no physical branches. Given that,neobanks differ from the classic ones, first of all, by their top-notch IT infrastructure. They offer almost all banking services online via desktop or mobile app.

There are two types of neobanks based on how they operate:

- a full-stack neobank;

- a front-end-focused neobank.

A full-stack neobank is a standalone bank with a banking license that operates completely independently.

A front-end-focused neobank doesn't have its own banking license and must connect to a BaaS and a bank partner that supports a neobank in terms of license, audit, etc.

Popular neobank examples

To keep it more practical and less theoretical, let's see how digital-only banks work based on the best neobanks in the US:

- Chime (20+ million account holders)

- Current (6+ million account holders)

- GreenFi (6+ million account holders)

Chime

Chime is a digital-only fintech company that partners with banks to offer checking and savings accounts. What makes their more than 20 million customers love them, though, is the absence of banking fees.

Chime has no monthly or overdraft fees, and it lets users round up purchases to the next dollar. Users can also earn up to 3.00% APY on savings, receive up to 1.5% cash back on purchases, and access more than 47,000 fee-free ATMs. But depositing cash can be expensive.

Current

Current is a neobank that isn't set up like a traditional bank with different account categories like checking and savings. Instead, Current offers hybrid accounts that combine checking and savings components. Current offers a cash-back rewards program, plus an interest rate of 4% on its Savings Pods up to $6,000.

Users can also receive their paycheck up to two days early through direct deposit, access fee-free overdraft, and advance up to $750 from an upcoming paycheck. The key drawback of Current is the lack of phone-based customer support.

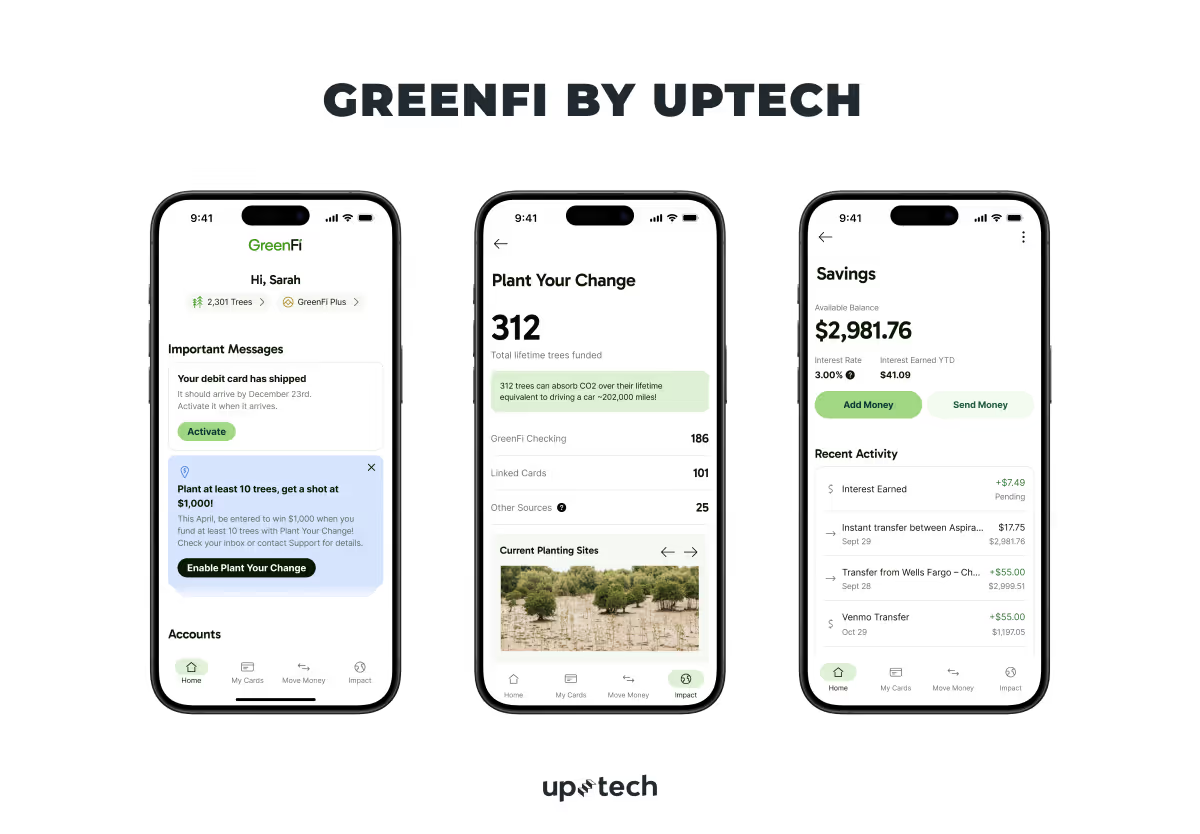

GreenFi

GreenFi is a climate-focused fintech platform that offers digital checking and savings accounts through partner banks. Uptech has worked with the GreenFi team for more than 10 years, supporting the development of their iOS and Android applications.

The platform offers typical digital banking features together with sustainability-oriented options. Users can receive their paycheck up to two days earlier through direct deposit, earn up to 3.25% APY on savings, and use the account without monthly or hidden fees. GreenFi also provides fee-free ATM access and up to 6% cash back when customers shop with selected climate-friendly brands.

What sets GreenFi apart is its environmental positioning. According to the company, customer deposits do not fund fossil fuel projects. Users can also choose options such as planting trees with purchases and offsetting their car’s emissions, while the app provides insights into the environmental impact of spending.

Learn more about our cooperation with GreenFi here.

How do neobanks make money?

Today, there are five business models for how neobanks earn money. I have rounded them up below. In practice, many neobanks rely on multiple revenue sources rather than a single one.

- Interchange-led model

This model relies on the revenue sourced through the interchange. Every time customers pay with the neobank's card, they get paid. Interchange fees are usually a small percentage of each card transaction paid by the merchant’s bank to the card issuer.

Example: Chime

- Credit-led model

This is a credit-first model. Neobanks using such a model start with a credit card or similar offering and then provide a bank account. Revenue mainly comes from interest on credit balances, late payment fees, and other lending-related charges.

Example: Nubank

- Ecosystem-led model

The checking account may not be the main profit driver in this model, but it unlocks a range of monetization strategies. Some neobanks also have monthly subscriptions as an additional monetization vector. Other revenue streams may include commissions from partner services such as insurance, investments, or financial marketplaces integrated into the app.

Example: Monzo

- Asset-led model

The asset-led model offers savings accounts and looks to obtain deposits with competitive rates. Some neobanks focus on ethical or moral spending management. Revenue can come from managing deposits, earning interest spreads, or offering additional investment and savings products.

Example: GreenFi

- Product extensions model

Credit-led models are distinctly successful but merely examples of product extensions, blurring the lines between financial domains. One of the biggest drivers here will come from more prominent tech companies and partnerships with banks.

These platforms often start with one financial product and gradually expand into accounts, cards, lending, or investment services.

Example: Robinhood

In many cases, the choice of business model depends on regulation, banking licenses, and partnerships with traditional banks. These factors often determine which revenue streams a neobank can legally operate and scale.

Why to Start a Neobank: Market Overview

Since we have done with the “what” part, it’s time for the “why it's beneficial to start a neobank” part.

If you're in a position to start a neobank, here are some real-world data points to show you that you're making a good decision.

First, the number of digital-only bank account holders in the USA is 52 million, which is one of the highest. Second, the number will grow due to the country's massive population and ability to boast some of the world's oldest digital-only banks. Overall, 80 million digital-only bank account holders will be in the US by 20258, making up an estimated 23% of the national population.

Neobanks represent a new approach to financial services, and it's no surprise that the rise of neobanks will be primarily supported by younger consumers.

Recent data from the American Bankers Association highlights how strongly younger generations rely on mobile banking. 64% of Gen Z and 68% of Millennials say they use mobile banking apps most often, compared with 55% of Gen X and 41% of Baby Boomers, who still tend to prefer online or PC banking.

Young generations and digital-only consumers will demand neobanks for several reasons:

- A customer-centric approach is at the core of neobanks.

- Financial services will become cheaper, simplified, and more useful.

- New, innovative features.

Neobank startups that bring significant value to customers (e.g., neobanks focused on the middle class who benefit from lower costs) and build a strong standalone unit economics will succeed in the fintech market.

Data from the FDIC also highlights the remaining market opportunity. About 14.2% of U.S. households (around 19 million) are underbanked, meaning they rely partly on alternative financial services, while 4.2% (about 5.6 million households) remain unbanked and do not have a bank account at all.

How to Start a Neobank: 8 Main Steps

Thankfully, you don't need to own a bank to start a neobank. What can be handy is being engaged in the fintech community, understanding how neobanks work, and getting equipped with a dedicated and professional development team.

We can help with the latter one. The Uptech team has successfully helped to launch five neobanks. We know how to start a digital bank first-hand. Here are some general guidelines from my experience and some tips I gathered from the Uptech team on how to start a neobank that brings value and profit.

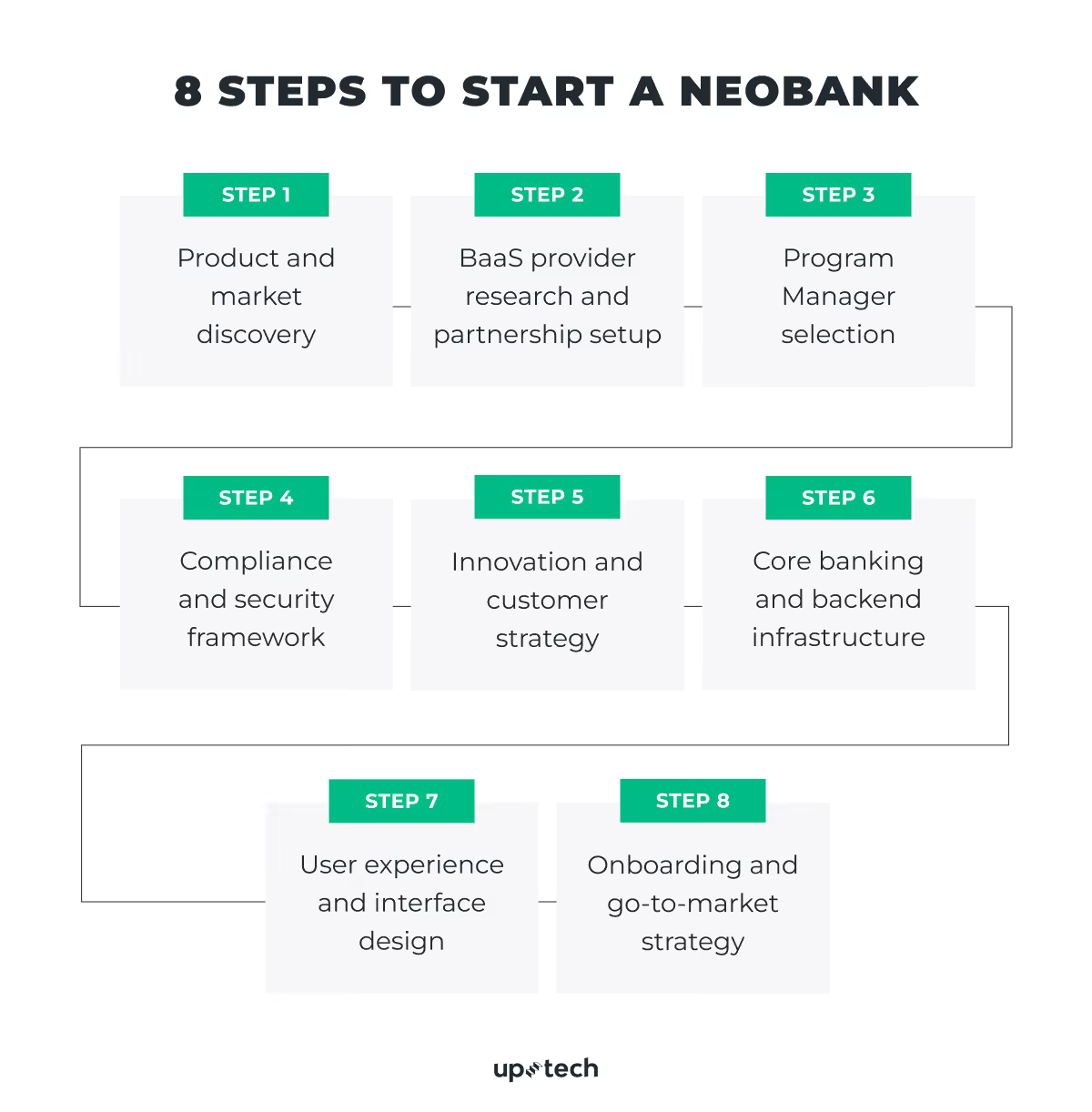

Basically, to launch a neobank, you will need to follow these 8 steps:

- Product and market discovery

- BaaS provider research and partnership setup

- Program Manager selection

- Compliance and security framework

- Innovation and customer strategy

- Core banking and backend infrastructure

- User experience and interface design

- Onboarding and go-to-market strategy

Before you start building a neobank, define the market you want to enter and whether you will launch through a sponsor bank / BaaS partner or work toward your own licensing path later. That choice affects your product scope, compliance requirements, and timeline.

Step 1: Conduct the discovery

I need to stress this more: with in-depth product and market discovery, your product is more likely to be successful. So start with:

- Defining your target audience & value proposition

- Identifying and analyzing audience pain points

- Analyzing your competitors and their pain points

We at Uptech are the ambassadors of Product Discovery and never miss it in the product development process. If you need help with discovering the neobanking market and shaping your value proposition, we are here to help.

Product Challenge: Choose the right business model

Choosing the right business model means keeping your neobank business profitable. Moreover, it would be great to foresee such circumstances and change the business model before you actually reach the stage where you’re operating at a loss.

Uptech Solution

The smartest way to choose the right business model is to analyze your consumers, define their behavior and determine the best way for them to use your product. We do all of the above during the Discovery stage. Once we know that, it’s easy to pick the business model (or combine several) that suits your business best.

Expert tip: Take the time to define your target audience and value proposition, identify and analyze pain points, and thoroughly research your competitors. This discovery phase is crucial for ensuring your neobank finds its product/market fit.

Step 2: Research and communicate with a BaaS provider

The second thing you should do is find a reliable BaaS provider. Ok, you may ask: what is BaaS? A BaaS (Banking-as-a-Service) is a service that connects fintech companies with licensed banks through APIs. This setup allows a neobank to offer services such as accounts, payments, and cards without holding its own banking license, because the regulated partner bank provides the underlying financial infrastructure.

Neobanks can use BaaS APIs to enable users to hold funds, pay bills, manage cash flow, loans, and access funding directly from the software.

In most neobank setups, the BaaS provider supplies infrastructure and APIs, while a licensed partner bank holds deposits and issues cards. Together, they enable the neobank to offer regulated financial services without becoming a bank itself.

At this stage, you should also define your launch jurisdiction and partner-bank model, because requirements differ by market and by product type.

Examples of BaaS and embedded-finance providers include, but are not limited to:

- Galileo

- Bond

- Unit

- Treasury Prime

- OpenPayd

- Solaris Group

It's critical to have technical research on your potential BaaS provider to know their terms and check if they match your requirements. For example, you need to have KYC embedded and offer a crypto account, but the BaaS you chose doesn't provide this functionality.

So check the terms attentively and then make your relationship with BaaS official. State all the terms of your collaboration to the smallest details because it's time when your neobank can officially provide financial services.

It is also worth defining early who will own reconciliation, fraud workflows, dispute handling, and customer support responsibilities.

Expert tip: Conduct technical research to ensure the BaaS provider's terms align with your requirements, such as KYC capabilities and crypto account support. Establish a solid relationship with your chosen BaaS provider for seamless collaboration.

Step 3: Decide who'll be your Program Manager

It can be an issuing bank, BaaS, or you. The role of a Program Manager includes a list of responsibilities:

- Direct relationships with certain networks;

- Web/mobile app development and ongoing maintenance;

- Marketing/Promotions/Advertising/Branding;

- Cardholder Communications;

- Customer Service;

- Compliance;

- Legal/Regulatory monitoring;

- Audits.

The list is far longer, but the point is that the Program Manager role is critical and must be clearly defined early in the project. If you look at the footers on the websites of Chime, you'll see that it issues through The Bancorp Bank, and GreenFi issues through Coastal Community Bank.

But it takes several months to get a deal with a bank. Meanwhile, you can collaborate with companies like Rise and mBank, which can be a Program Manager for you.

Step 4: Ensure compliance and security

Many neobanks are not licensed banks themselves. It is the bank with which the neobank is partnering that is the regulated institution. The partner banks are regulated by the examiners.

During the audits and regulatory exams, these partner banks must prove that they comply with certain standards and security practices. The neobank needs to adhere to the standards of the bank it is working with, which makes the partner bank a quasi-regulator for the neobank.

Your BaaS provider can support you and provide a toolkit to help build a top-notch compliance program.

Product Challenge: Provide a secure solution

Providing neobanking app security means taking steps to protect the user’s account and data. It’s often a challenge when a company doesn’t have a dedicated server/ data center or partners with unreliable third-party providers that hackers may attack.

Uptech solution

Third-party integrations are extremely helpful in the fintech sector, and we at Uptech have worked on 6 fintech projects where we had to integrate third parties. We researched dozens of providers and checked if they highlighted what data they used and for which purposes. And only after ensuring that the service is 100% compliant, we integrate it.

Uptech Note 📌

Regulatory frameworks and licensing requirements vary widely across jurisdictions and types of financial services. The choice of regulatory licensing depends on your value proposition and business model.

Step 5: Work on innovative, customer-centric strategies

This step isn't the one you should start cultivating only here. It's a 24/7 journey. The thing is that the neobank market demands new players to be innovative with their solutions. Otherwise, you'll lose.

That's because many startups push harder on the accelerator pedal as they grow and think innovation-first to buy future growth. Venture investors love this, as it allows them to return money to their baskets faster.

Expert tip: Stand out in the competitive neobank market by consistently cultivating innovative and customer-centric solutions. Emphasize an innovation-first approach and prioritize customer needs to drive future growth.

Step 6: Build a strong core and backend infrastructure

To build a secure and scalable neobanking app, it's necessary to select suitable components, including backend infrastructure, a tech stack, frameworks, and architecture. Developers with relevant skills and experience in fintech can help a lot here.

When selecting a backend tech stack, Uptech developers reckon with the following factors:

- product's specifications (type, business goal, size, complexity, etc.)

- project's timeline and budget

- requirements, such as transaction processing reliability, ledger accuracy, fraud monitoring, and audit readiness

Bearing the above factors in mind, we opt for the best-suited tech stack for your product.

Step 7: Focus on user-friendly design

If you open a banking app and are afraid to make a money transfer, the app design is probably poor. Why is that? Because banking apps should simplify and humanize things, not scare users away.

So, is there a formula for the neobanking app design that works?

Not really. But there's a way to recognize good neobanking app design from bad design. Good design is a perfectly balanced UX and UI. And you really need to hire a professional UX&UI designer to nail both to create a killer app that people will love. UI should have clear fonts and nice colors, and other app elements should create the general style. User experience has the ultimate goal – to keep a user engaged.

Product Challenge: Create a smooth user experience and build trust

Building trust with customers is about building confidence in your product, its value, and its security. In the case of neobank app development, getting the trust of your users requires two things: transparency and security.

Uptech Solution

To build trust through the neobanking app design, we provide users with really important information that is teachable, available, and easily accessible when they need it:

- We make terms of use and privacy policies explicitly presented during onboarding and easy to access later in the app

- We ask permission for any data the app collects and articulate it very well

- We provide clear steps explaining each and every piece of data we’re asking for

- We make pricing options transparent, don’t hide any fees, and communicate any changes in advance

- We broadcast the regulatory compliance, show information on the certification, adopt AML/KYC policies, and so on

Step 8: Ease onboarding and go-to-market strategy

Onboarding, user engagement, and marketing, while technically the last steps in the neobanking app development, are often the ones most overlooked by startup founders and business owners.

Creating a fintech product means you're dealing with sensitive information of your customers, so it's important to think about how to create a neobank app as intuitive, user-friendly, and easy to use as possible. Then build your own onboarding and go-to-market strategy to supplement it.

Before a full launch, many fintech teams also run internal testing and limited pilot programs to validate onboarding flows, KYC success rates, card activation, fraud monitoring, and support processes in real conditions.

Neobank Features to Stand Out

Here, I gathered the must-have neobank features and added a few to help you stand out in the fintech market.

Must-have neobank features

Sign up/ Sign in. Users need a simple and secure way to create an account and log in. Most neobanks combine email or phone authentication with additional security layers such as OTP codes.

Biometrics. Biometric authentication, such as fingerprint or Face ID, allows users to access their accounts quickly and securely without entering passwords every time.

KYC. Know Your Customer verification confirms a user’s identity before they can access financial services. This process usually includes document verification, identity checks, and fraud screening.

Home page. The home screen is the central dashboard where users can view balances, recent transactions, cards, and shortcuts to key actions. So it deserves your special attention.

Checking (Spending) account. This is the main account users rely on for everyday transactions such as payments, transfers, and card purchases.

Saving account. As the name suggests, savings accounts help users store money and often provide interest or automated saving tools to encourage better financial habits.

Debit card. A debit card connects directly to the user's account and allows them to pay online, in stores, and withdraw money from ATMs.

Block/Unblock card. Users should be able to instantly freeze or unfreeze their debit card from the app in case of suspicious activity or a lost card.

Change PIN. The app must allow users to securely update their card PIN without contacting support.

Report card lost. If a card is lost or stolen, users need a quick way to report it and request a replacement.

Support. Often underestimated, in-app support or chat allows users to quickly resolve issues related to payments, transactions, or account access.

Neobank features to stand out

Cross-border payments, including crypto. These features allow users to send and receive money internationally. Some neobanks also support crypto transfers or wallets to simplify global transactions.

Cross-border deals offer growth for both businesses involved and the users. Pooling the incomes generates more revenue for both companies. More revenue means greater financial power, which in turn means a privilege over competitors and an extra benefit for users.

Budgeting assistance. Budgeting tools categorize spending, track expenses, and help users understand where their money goes. Many apps also provide insights or recommendations to improve financial habits.

Consumer-friendly neobanking apps offer a full suite of services and promote financial literacy. It's all about more value to your users.

Payments through QR Codes. QR payments allow users to send or receive money by scanning a code. This method is fast, requires no card or account number input, and is widely used in mobile-first payment ecosystems.

Payments through QR codes are surging. From a business point, it's a new way to reach customers and facilitate payments. From the users' point of view, it's so accessible, easy, and friendly.

Micro-investment. These tools allow users to invest small amounts of money, often automatically. Some apps round up purchases and invest the spare change.

Gen Z wants financial apps that are customized to their lives and needs. Micro investment is among those needs.

Impact Score. An impact score measures how a user’s spending affects environmental or social factors. For example, some neobanks estimate carbon emissions associated with purchases and suggest ways to offset them.

Sustainability in fintech is one more awesome trend. For example, GreenFi users can measure their climate impact based on their expenses/ investments.

We offer full-cycle financial software development services, from creating a product development strategy to top-notch fintech services implementation. Create, develop, and design your fintech software with Uptech 🚀

How to Develop a Neobank: Uptech Case

It's a pleasure to say that we at Uptech had a chance to create five awesome neobank apps. One of them is GreenFi, a U.S.-based fintech platform that focuses on sustainable banking.

Uptech started working with the GreenFi team in 2016, helping them turn an early product concept into a full-featured digital banking platform. Over the years, our team supported the development of iOS, Android, and web applications, built core financial features, and helped scale the product while maintaining strong security and reliability standards.

GreenFi challenge: Build a secure and scalable fintech platform

GreenFi handles sensitive financial and personal data, which makes security and stability critical. At the same time, the product continues to evolve with frequent feature updates and UI improvements. The team needed a technology partner that could support rapid development while maintaining high standards for security, testing, and system stability.

Uptech solution

Our engineering team helped build and maintain the core application infrastructure while introducing processes that support long-term scalability and reliability.

To support this goal, we:

- Implemented multi-factor authentication, biometric login, and encryption to protect user accounts and sensitive financial data;

- Integrated Plaid for external account linking and Stripe for direct funding

- Built an AI-powered receipt scanning tool to extract transaction data automatically

- Integrated Apple Pay wallet provisioning for convenient mobile payments

- Implemented automated testing, including unit, screenshot, and end-to-end tests

- Introduced real-time monitoring with DataDog to detect unusual behavior and system issues early

In addition to the technical infrastructure, our team helped develop core product functionality, including:

- spending and saving accounts

- cashback rewards from ethical brands

- carbon footprint tracking for transactions

- micro-donations and tree planting integrations through Veritree

- The Plus membership program offers additional financial benefits

As a result of this long-term collaboration, GreenFi evolved into a full-featured fintech platform that combines digital banking tools with sustainability-focused features.

"They provide high-quality work very responsibly — we’ve built a strong relationship and get along well."

Matt Lee, GreenFi Head of Product

How Much Does It Cost to Start a Neobank with Uptech?

The cost of developing a neobank depends on numerous factors: the app's complexity, whether you need to polish the existing app or build a new one from scratch, the team engaged, and the outsourcing partner's location.

At Uptech, we offer several options:

- Developing a neobank from scratch and starting with the MVP

- Rebuilding the existing app and extending the feature base

- Polish the existing app by improving some parts of it

The timeframe for each case is different, which means costs vary too. On average, it takes us 5-7 months to develop a functioning MVP.

To develop the fully-functional app, you'll need the project team, which includes:

- Project manager

- UX designer

- Back-end developers

- Front-end developer

- QA engineers

The average hourly rates at Uptech range between $40-$70 per hour, depending on the role and project scope.

Based on a typical fintech product team and a 5–7 month MVP timeline, the estimated cost of building a neobank MVP usually falls between $120,000 and $350,000.

Of course, the final cost depends on factors such as the number of platforms (iOS, Android, Web), integrations with banking providers, security requirements, and the feature set.

If you want to get a quick ballpark estimate before talking to the team, you can also use our app development cost calculator. It allows you to estimate the potential budget based on the platform you choose and the features you plan to include.

Developing a neobank is an incredible journey, full of opportunities, as the market is on the rise right now. On the other hand, you should be ready for the challenges, such as app security, innovation, and the use of top-notch technologies.

If you're exploring how to start a neobank or want to estimate the cost of building one, the Uptech team can help you validate your idea, define the scope, and plan the development roadmap.

Contact our team to share your idea, and we'll be happy to help.

FAQs

How to build a neobank from scratch?

The Uptech team has successfully helped to launch five neobanks. We know how to start a neobank from scratch. Here are some general guidelines from our experience on how to start a neobank that brings value and profit:

- Conduct the discovery

- Research and communicate with a BaaS provider

- Decide who'll be your Program Manager

- Ensure compliance and security

- Work on innovative, customer-centric strategies

- Build a strong core and backend infrastructure

- Focus on user-friendly design

- Ease onboarding and go-to-market strategy

How do neobanks make money?

There are five business models for neobanks to earn money. I have rounded them up below:

- Interchange-led model – This model relies on the revenue sourced through the interchange.

- Credit-led model – This is a credit-first model.

- Ecosystem-led model – Some neobanks also have monthly subscriptions as an additional monetization vector.

- Asset-led model – The asset-led model offers saving accounts and looks to obtain deposits with competitive rates.

- Product extensions model – Credit-led models are distinctly successful but merely examples of product extensions, blurring the lines between financial domains.

How much does it cost to start a neobank?

The cost of developing a neobank depends on numerous factors: the app's complexity, whether you need to polish the existing app or build a new one from scratch, the team engaged, and the outsourcing partner's location.

The timeframe for each case is different, which means costs vary too. On average, it takes 3-5 months to develop a functioning MVP, and the project team needed includes:

- Project manager

- UX designer

- Back-end developers

- Front-end developer

- QA engineers

The average hourly rates at Uptech are $40-70. If we do the math, we’ll get $120,000-$360,000 as the average cost of building a neobank app.