Fintech is changing fast. Digital-first models, embedded finance, and new consumer habits are rewriting how the field moves. But with growth comes pressure: more regulations, rising fraud, and higher customer expectations.

The industry is already leaning on AI to manage this. A recent report stated that 75% of financial companies use artificial intelligence, and another 10% plan to adopt it soon. This makes one thing clear to business leaders: AI and machine learning are setting the standard for competition.

ML plays a double role. On one side, it’s a shield that protects against fraud, supports compliance, and reduces risk. On the other hand, it’s a growth driver — powering personalization, smarter credit scoring, and scalable operations. Together, these make ML the engine behind the next wave of fintech innovation.

I’m Oleh Komenchuk, ML Lead at Uptech. In this article, I’ll show how ML helps fintech solve some of its biggest challenges.

Let’s get started.

Core Challenges in Fintech that Machine Learning Can Solve

AI and ML are everywhere in a modern business field. Decision-makers and business strategists are experimenting with them in products, operations, and strategy. Amidst all this buzz, it’s important to remember that AI is not a universal problem solver. The intention to apply it should be backed by research, collective brainstorming, and a solid “why it’s the right fit”.

That doesn’t mean experimentation is off the table. Innovation often starts with testing new ideas. However, sticking to tried-and-true paths means fewer risks and a clearer idea of what benefit you’ll get in return.

Here are some of the ways machine learning is already driving an impact.

How ML helps fight fraud and cybersecurity threats

Fraud remains the biggest threat to fintech’s profitability and reputation. According to Alloy’s State of Fraud Report, nearly 33% of financial organizations suffered direct fraud losses over $1 million in 2025 — up from just 25% in 2024. Meanwhile, a 2024 Recorded Future report shows 269 million card records and 1.9 million bank checks were exposed on dark/clear web platforms, indicating the rising scale of data fueling fraud attacks.

The challenge is structural. Transactions in banking move nonstop — many settle within seconds — leaving an incredibly narrow window to detect anomalies. Fraudsters also evolve fast: old tactics like account takeovers and synthetic IDs now coexist with cross-border mule networks, “fraud-as-a-service” kits, and even AI-generated attacks that can fool static, rules-based systems. For digital-first institutions, one breach can trigger regulatory fines, loss of trust, and years of reputational recovery.

Machine learning in the fintech industry provides a dynamic line of defense — one that learns, adapts, and improves with every transaction.

Anomaly detection

Think of anomaly detection as teaching the system what “normal” looks like for every customer, merchant, or type of transaction. For example, if you usually buy groceries in your hometown, the system learns that pattern. If one day there’s a sudden $5,000 jewelry purchase from another country on your card, that looks abnormal.

Unlike old fraud systems that rely on hard rules (like “block anything above $2,000”), ML doesn’t freeze at a fixed threshold. Instead, it continuously learns and adjusts, comparing each new transaction against past behavior in real time. That way, it can flag unusual activity without blocking legitimate variations, like you making a higher purchase during the holidays or while traveling.

Anomaly detection works best when it continuously learns from context, so it doesn’t overreact to natural changes in user behavior.

Behavioral biometrics

Passwords and one-time codes can be stolen, guessed, or phished. ML goes further by watching how a person interacts with their device. It tracks subtle, almost invisible patterns like how fast someone types, the rhythm of keystrokes, the pressure of their taps on a touchscreen, the way they move a mouse or swipe, or even how they hold a phone using built-in sensors.

These signals are unique and very hard for fraudsters to mimic. By comparing current behavior to a user’s past profile, ML can silently confirm identity during a session, without forcing extra logins or codes.

The big advantage is that these checks happen in the background, reducing account takeover risk without adding friction for genuine customers. The nuance is that no single signal is perfect, so systems usually combine multiple behavioral indicators with device and location data to avoid false alarms.

Cross-channel learning

Fraud rarely happens in isolation — it spreads across payment types, devices, and even different financial apps. Traditional, rules-based systems often treat each channel separately (cards, bank transfers, wallets), which means they can miss the bigger picture.

ML solves this by connecting activity across channels and geographies. For example, it might notice that the same email address is tied to multiple accounts, all using different cards, but logging in from the same device or IP address. Or it might detect that funds are being moved through a chain of “mule” accounts in several countries before disappearing.

Because ML can process vast amounts of data in parallel, it spots patterns and fraud rings far faster than human analysts or manual rules ever could. This network-level view is especially powerful for uncovering coordinated schemes that look harmless when viewed transaction by transaction.

The nuance is that cross-channel learning requires careful data integration and privacy controls — financial companies must ensure they’re allowed to combine and analyze signals from different products and regions while staying compliant with regulations like GDPR.

Real-world example: PayPal has publicly acknowledged its use of advanced AI/ML to counter increasingly sophisticated fraud attacks. In an interview with the Associated Press, PayPal’s Chief Product Officer explained how the firm uses algorithms to detect “complex fraud patterns in real time,” enabling it to intervene swiftly. Together with its long-standing investments in behavioral modeling, device intelligence, and ensemble risk systems, these methods help PayPal maintain relatively low fraud losses while scaling transaction volume.

How ML supports compliance and AML/KYC

KYC (Know Your Customer) is a process that verifies a customer's identity at onboarding by checking documents, addresses, and other relevant data. The goal is to prevent fraudsters and sanctioned individuals from accessing the financial system.

AML (anti-money laundering) is the ongoing process of monitoring transactions to prevent criminals from disguising “dirty” money as legitimate. This includes identifying suspicious activity and reporting it to the relevant regulators.

Together, AML and KYC form the backbone of financial integrity. Done right, they build trust with regulators, investors, and customers alike. Done poorly, they create vulnerabilities that criminals exploit and regulators punish.

In 2024, regulators globally issued $4.6 billion in enforcement penalties tied to AML, KYC, sanctions, and transaction monitoring failures.

The problem runs deeper than fines. Traditional AML systems generate up to 95% false positives, creating enormous noise in compliance workflows.

At the same time, regulators are raising expectations — AMLD5 in the EU requires stronger transaction monitoring, while PSD2 mandates real-time payment authentication. In the US, the SEC and FinCEN are tightening scrutiny on digital-first platforms.

Machine learning applications in fintech help automate and strengthen regulatory processes, making compliance faster, more accurate, and less resource-intensive.

Automated identity verification

Onboarding new customers often means verifying passports, driver’s licenses, or other official documents — a process that can be slow and error-prone if done manually. ML makes this far faster and more reliable. Using OCR (optical character recognition) and computer vision, systems can instantly read and verify the details on an ID, detect tampering, and confirm the document's authenticity.

But it doesn’t stop at the documents. ML can cross-reference the extracted data against government watchlists, sanctions databases, or internal risk lists within seconds. If something doesn’t match — for example, the photo appears altered or the name is associated with a flagged individual — the system can immediately raise an alert.

For the customer, this means faster onboarding and a smoother journey. For the company, it reduces manual review costs and strengthens compliance with KYC/AML regulations.

While fintech machine learning projects greatly improve speed and accuracy, they still need human oversight for edge cases (like unusual documents, poor image quality, or high-risk matches). The best setups use ML for the bulk of checks, with human reviewers handling the complex exceptions.

False positive refinement

One of the biggest challenges in compliance is the flood of alerts that turn out to be false alarms. In fact, in many legacy systems, up to 98% of alerts never result in a real issue. That means analysts spend most of their time chasing noise instead of stopping genuine risks.

ML helps by scoring and prioritizing alerts more intelligently. Instead of treating every match the same, it examines the broader context, such as transaction patterns, customer history, and links to other entities, to determine whether an alert is worth investigating. This dramatically cuts the number of unnecessary alerts.

The impact is twofold:

- Operational costs drop because fewer hours are wasted on dead ends.

- Analysts can focus on high-probability cases, improving both speed and accuracy of investigations.

ML doesn’t eliminate false positives entirely: regulators still expect cautious checks, but it brings the volume down to a manageable level, transforming compliance from a box-ticking exercise into a risk-focused function.

Entity resolution and network analysis

Financial crime often hides in the gaps — the same individual may open accounts under slightly different names, use multiple email addresses, or spread activity across several platforms. Traditional systems struggle to connect these fragments, which lets fraudsters and money launderers slip through.

ML helps by performing entity resolution: pulling together scattered records (different spellings of a name, multiple phone numbers, variations in address) into a single, unified view of the customer or account. This prevents criminals from appearing as multiple “clean” individuals in the system.

When combined with graph-based ML, the picture becomes even more powerful. Graph models map the relationships between entities — accounts, devices, counterparties, or regions — and highlight unusual clusters or hidden links. For example, a network of seemingly unrelated accounts may all funnel money to the same offshore beneficiary.

This approach can expose laundering rings that operate across borders and payment channels, something rule-based systems almost never catch.

Entity resolution must balance accuracy and privacy: merge records too aggressively and you risk false matches; too cautiously and you miss real links. That’s why most financial institutions pair ML-driven matching with human validation for the riskiest cases.

Real-world example: HSBC’s experience offers one of the clearest real-world demonstrations of how ML can transform anti-money laundering (AML) operations. In partnership with Google Cloud, HSBC leveraged AI/ML enhancements to its transaction monitoring systems. The revamped platform now processes more than 1.2 billion transactions per month, applying advanced algorithms to filter, triage, and prioritize alerts.

How ML improves risk management and credit scoring

Traditional credit scoring was built for a different era. Most legacy models still rely on a handful of fixed data points: repayment history, outstanding debt, and the length of someone’s credit file. While these metrics can work reasonably well for salaried individuals in mature banking markets, they leave out huge segments of today’s financial world.

- “Thin-file” customers. Freelancers, gig workers, immigrants, and young adults often lack the long paper trails that traditional scores depend on. As a result, they are unfairly penalized or excluded.

- Emerging market populations. In many parts of the world, large groups of people don’t have access to formal banking at all, which means billions remain “unscored” and locked out of credit opportunities.

- Dynamic lifestyles. Modern consumers don’t fit into the old mold — they change jobs frequently, juggle multiple income streams, or even relocate to new countries. Static scoring systems can’t keep up with this fluid reality.

The result is widespread credit exclusion. According to the World Bank, 1.4 billion adults remain unbanked globally. For lenders, this represents both a growth ceiling, as fewer customers are within reach, and a blind spot in risk, since there’s little insight into which members of the “unscored” or underwritten population are actually creditworthy.

Machine learning helps financial institutions assess risk more accurately, respond faster to changing borrower behavior, and make better credit decisions at scale.

Alternative data integration

One of the biggest strengths of ML in credit scoring is its ability to go beyond the narrow set of traditional bureau data. Instead of looking only at loans and credit cards, ML models can incorporate non-traditional signals such as mobile phone usage patterns, utility bill payments, rent history, e-commerce installment repayments, and even psychometric tests that measure traits like reliability or risk-taking.

For example, a freelancer who doesn’t have a long credit card history might look “invisible” to a conventional score. But if the same person consistently pays rent on time, keeps up with utility bills, and demonstrates stable income flows through digital wallets, ML can flag them as low risk.

This richer view helps lenders open access to credit for underserved groups while still managing risk effectively. However, data quality and privacy rules matter: not every alternative signal is reliable or allowed in every jurisdiction, so models must be carefully designed to stay compliant.

Bias detection and fairness

One of the biggest criticisms of traditional credit scoring is its lack of transparency. Legacy models often function like black boxes, and because they lean so heavily on historical data, they can unintentionally reproduce old biases — unfairly penalizing people based on race, gender, ZIP code, or socio-economic background.

ML offers a way forward. Modern frameworks can be audited for bias: regulators and risk teams can run fairness tests, compare outcomes across demographic groups, and adjust models when disparities appear. For example, if a model consistently undervalues applicants from certain neighborhoods, bias-detection tools will flag it so that features can be reweighted or redesigned.

This isn’t just an ethical responsibility — it’s also a regulatory expectation. Laws in the U.S. (Equal Credit Opportunity Act), the EU’s AI Act, and many local banking regulations require financial institutions to prove that their models treat customers fairly.

Remember that no ML model is bias-free by default. Fairness requires ongoing monitoring, governance, and human oversight — but unlike legacy systems, ML makes these checks visible and actionable.

Portfolio-level optimization

Credit risk isn’t just about judging individual borrowers — it’s also about managing the health of the entire lending book. At scale, ML gives lenders the ability to dynamically adjust credit exposure across demographics, markets, or product lines.

For example, if models detect rising default signals in a specific region or income group, credit limits can be tightened proactively. Conversely, if another segment shows strong repayment behavior, exposure can be expanded to capture growth. This constant balancing act helps lenders avoid dangerous concentrations of risk while still pursuing new opportunities.

For fintech lenders in particular, this capability is critical when expanding into new geographies or launching new products. ML enables them to test markets with tighter controls, learn quickly from repayment data, and scale only where the portfolio remains healthy.

The nuance is that portfolio-level optimization requires alignment with business strategy and compliance — too much automation without oversight could lead to unintended exclusions or regulatory scrutiny. The most effective lenders pair ML-driven insights with human judgment in capital allocation decisions.

Real-world example: JPMorgan created a proprietary AI/ML-powered risk indicator called the Account Confidence Score, which evaluates the likelihood that a destination account is safe before a payment is released. The system draws on signals such as prior fraud associations, transaction history, and frequency/recency of activity, combining them into a single confidence score that treasurers see in their workflow.

By embedding ACS directly into corporate payment systems, JPMorgan enables clients to pre-screen beneficiary accounts and proactively block suspicious transfers. This effectively shifts risk management upstream, helping prevent fraud before funds leave the bank, while complementing existing fraud detection and KYC controls.

How ML powers customer experience and personalization

In consumer finance, the “products” themselves are nearly indistinguishable. Every bank offers some combination of cards, savings, loans, and payments. What sets winners apart is not the menu, but the experience wrapped around it. Customers now expect their bank to anticipate needs as intuitively as Netflix or Amazon: instant, predictive, and relevant.

Machine learning applications in the fintech industry help companies go beyond one-size-fits-all services, understand individual needs, personalize interactions, and build stronger, long-term relationships.

Hyper-personalized recommendations

ML makes this possible by combining transaction history, demographic information, and behavioral patterns to predict what each customer actually needs next.

Instead of blasting the same generic credit card offer to everyone, ML enables tailored, “next best product” recommendations, such as a travel rewards card for a customer who frequently books flights and hotels, a credit-builder loan or secured card for a thin-file user just starting their financial journey or a high-yield savings account for someone who consistently has extra money left at the end of each month.

This level of personalization turns every customer interaction — whether in-app, via email, or at checkout — into a potential conversion opportunity. It boosts relevance, strengthens loyalty, and increases the lifetime value of each customer.

Predictive financial coaching

One of the most powerful uses of ML in fintech goes beyond fraud prevention or credit scoring — it’s about helping customers manage their money better in real-time. By analyzing transaction flows and behavior, ML models can anticipate customer needs before they are even asked.

For example, if the system notices that upcoming bills are likely to exceed a user’s balance, it can flag the shortfall in advance and offer a micro-credit line or a flexible payment option.

This kind of proactive coaching elevates the brand from being just a service provider to becoming a trusted financial advisor. It deepens engagement, builds loyalty, and positions the platform as a long-term partner in the customer’s financial journey. Predictive coaching must be handled carefully: advice should feel supportive, not judgmental, and transparency about how recommendations are generated is key to maintaining trust.

Conversational AI and 24/7 support

Chatbots and voice assistants powered by natural language processing are now capable of resolving the majority of routine customer requests, such as checking balances, resetting passwords, or disputing transactions. For many companies, this means up to 80 percent of tier-one queries can be handled automatically.

The real benefit goes beyond cost savings. Customers get instant, always-on service without waiting in a call queue or navigating clunky menus, which directly improves satisfaction and reduces churn. Unlike static FAQ-style bots, modern ML-powered assistants don’t stay frozen at launch. They continuously learn from each conversation, expanding their knowledge base and becoming more accurate and helpful over time.

This turns customer support from a reactive cost center into a proactive engagement channel, where users feel heard, supported, and connected to the brand whenever they need help.

Personalized spending insights and nudges

Machine learning can automatically categorize spending in real time and transform raw transaction data into meaningful, personalized insights. Instead of simply listing charges, the system can point out that a customer spent 25 percent more on dining this month compared to their six-month average, or highlight that at their current savings pace, they are only fourteen months away from a down payment goal.

These timely nudges do more than inform. McKinsey reports that companies that excel at personalization often see 10–15 % revenue uplift and strong customer outcomes from personalization efforts. At the same time, customers tend to check in more often, which drives higher engagement and daily log-ins.

The key is subtlety. When presented as helpful suggestions rather than heavy-handed instructions, spending insights become a tool for empowerment, deepening trust and making the financial app part of a customer’s everyday routine.

Real-world example: Capital One’s Eno Assistant is one of the best-known ML-driven financial chatbots. Eno proactively alerts customers about duplicate charges, free trials converting to paid subscriptions, or unusual spending patterns. This AI assistant has shifted Capital One’s customer engagement from a reactive service to proactive financial coaching, strengthening loyalty while reducing call center loads.

How ML drives operational efficiency

Fintech companies are designed to be lean and agile, but their growth creates operational paradoxes. Every new customer, transaction, and regulatory requirement adds invisible “back-office gravity” — reconciliation, reporting, compliance checks, contract reviews, dispute resolution, and data ingestion. Unlike fraud or CX, these aren’t headline problems, but left unaddressed, they quietly choke scalability and margins.

- For a digital bank processing millions of transactions per day, manual reconciliation costs can consume up to 10–15% of operating expenses.

- Regulatory reporting requires teams to generate accurate, auditable filings under strict deadlines — failure risks fines or reputational damage.

- Loan servicing, invoice processing, and document verification grow in proportion to customer volume, forcing many companies to add headcount linearly just to maintain operations.

This ruins the very advantage fintech projects promise investors: scale without bureaucracy. The cost-to-income ratio, a key efficiency benchmark, often balloons as companies move from early growth to mid-stage maturity.

Operational automation is another standout among machine learning use cases in fintech. ML drives efficiency through automating repetitive workflows, forecasting demand, and freeing teams to focus on strategic, high-value work.

Intelligent process automation in operations

The biggest efficiency gap often hides in plain sight — routine, rule-based tasks that still depend on manual review. Loan servicing, compliance checks, or reconciliation workflows may look simple on paper, but together they consume massive time and introduce costly delays.

Machine learning changes that by connecting previously fragmented processes into a single, intelligent system. Instead of automating individual steps, ML-driven platforms coordinate entire workflows end-to-end. They classify incoming data, predict which cases are straightforward, and route those automatically, while flagging complex or high-risk ones for expert review. This keeps human focus where it adds the most value — on judgment and exceptions, not repetition.

The difference is scale and precision. Operations that once grew linearly with headcount can now expand without extra staff. Each automated action is logged and traceable, creating built-in compliance transparency rather than after-the-fact reporting. Over time, the system also learns from outcomes — refining how it prioritizes, sequences, and distributes work across teams.

Predictive workload management

Machine learning in fintech isn’t only about automation — it also helps leaders see around the corner. By analyzing historical patterns alongside external signals, ML can forecast when demand will surge and where resources will be stretched.

For example, support teams often face seasonal spikes in inquiries around tax deadlines, holiday shopping, or new product launches. Transaction volumes may climb sharply during travel seasons or promotional campaigns. With predictive models, businesses can anticipate these peaks, ensuring the right number of staff or cloud resources are in place ahead of time.

This foresight avoids the risks of overstaffing, which drives up costs, and bottlenecks, which frustrate customers. It also enables smarter scheduling, smoother service delivery, and ultimately a more resilient operation. Forecasts aren’t perfect — unexpected events (like outages or fraud waves) still happen — so predictive models work best when paired with flexible staffing and contingency playbooks.

Real-world example: Private equity firm Presidio Investors faced a familiar yet costly problem: excessive time spent on manual back-office tasks. Their team sifted through endless investment documents, emails, and attachments, parsing numbers, names, and charts, and then uploaded the data into their CRM manually. The process was slow, error-prone, and a major drag on scalability.

Working together, we built an AI-powered workflow that turned this bottleneck into an efficiency engine. Using OCR and NLP, the system could read and extract data from PDFs, Word files, and even scanned images, converting everything into structured formats ready for automatic CRM entry. To ensure compliance and security, the solution ran in a private cloud setup, keeping sensitive financial data protected.

The impact was dramatic:

- 80% reduction in manual work.

- Capacity to process up to 100 deals per day.

- Faster, cleaner insights, letting Presidio’s team focus on analysis instead of data entry.

Curious how it worked in detail? Read our case study here.

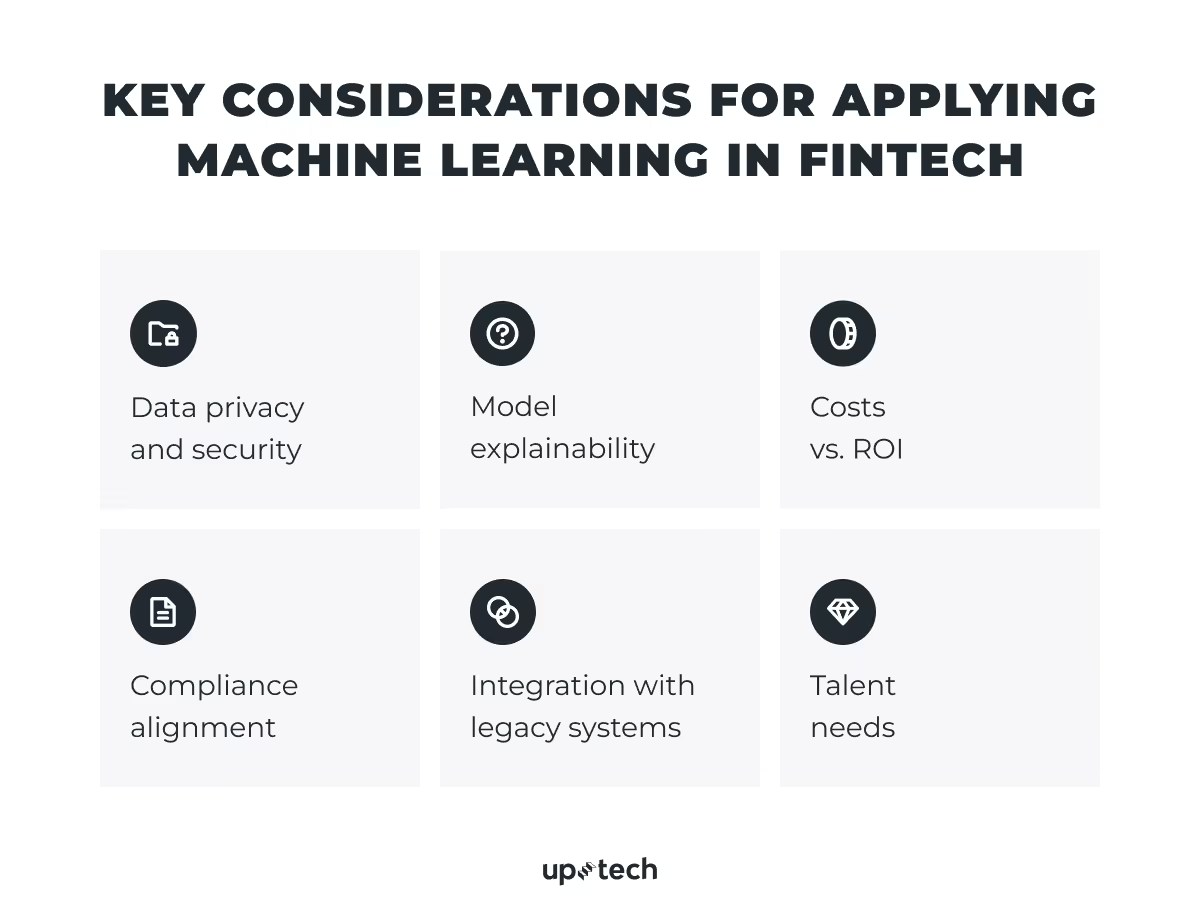

Key Considerations for Applying ML in Fintech

While machine learning can solve major operational and strategic challenges, its implementation in finance comes with its own complexities. The technology operates within one of the most tightly regulated, data-sensitive environments in the world, meaning every innovation must balance speed with responsibility.

Below are several practical factors fintech leaders should account for before scaling ML initiatives.

Data privacy and security

Financial services deal with the most sensitive kind of personal data — names, addresses, account balances, transactions, and even location patterns. Laws like the GDPR in Europe and the CCPA in California strictly govern what can be collected, how long it can be retained, and with whom it can be shared.

For fintech companies, this means ML projects can’t simply “grab all the data and train a model.” Every step — from gathering training data to storing outputs — must respect consent and minimization principles. A customer should know why their data is used, and companies must prove it’s stored safely. A single breach or misuse isn’t just a reputational hit; it can lead to multi-million-dollar fines.

To manage this risk, ML systems should be built with privacy by design: encrypting sensitive fields, anonymizing personal identifiers, and maintaining clear audit trails to demonstrate regulatory compliance.

Model explainability

One of the toughest challenges in finance is the black box problem. Imagine an algorithm declines a customer’s loan but can’t explain why. That’s unacceptable in a regulated industry where decisions impact people’s lives.

This is why explainability is essential. Lenders must be able to point to specific reasons — for example, “your repayment history was too short” or “your income flow is inconsistent.” Tools like SHAP and LIME break down a model’s decision into human-understandable factors. Without this transparency, regulators may block deployment, and customers will lose trust.

To address this, fintech teams should embed interpretability frameworks early in model development rather than adding them as an afterthought, ensuring that every prediction can be justified, audited, and refined when needed.

Costs vs. ROI

Machine learning promises huge returns: fraud reduction, smarter lending, and lower manual workloads. But getting there isn’t cheap. Building production-grade ML requires:

- Specialized talent (data scientists, ML engineers, compliance officers)

- Infrastructure (secure cloud platforms, data pipelines, monitoring tools)

- Governance (model risk management, audit trails)

The upfront costs can be high, while the benefits often materialize over months or years. Smart fintech leaders weigh these investments against projected savings — for example, showing that reducing false fraud alerts by 30% saves millions in lost approvals.

A practical approach is to start small: run pilots on narrow, high-impact use cases, measure concrete results, and expand only when ROI is proven. This way, investment stays manageable and every next step is justified by data.

Compliance alignment

Financial services are one of the most regulated industries in the world. Any ML system must meet existing obligations like AML, KYC, fair lending rules, and, increasingly, AI-specific regulations.

For example, under the EU AI Act, credit scoring is classified as a “high-risk” application. This means companies must provide documentation, conduct regular bias testing, maintain audit logs, and ensure humans are “in the loop.” Deploying ML without aligning with compliance first isn’t just risky — it could halt operations entirely or attract heavy penalties.

To prevent this, compliance and technical teams should collaborate from the start, reviewing data sources, decision logic, and risk models before production. This early alignment helps avoid rework, ensures smoother audits, and builds confidence across both business and regulatory stakeholders.

Integration with legacy systems

Many financial institutions still rely on older core systems not designed for real-time ML. Integrating new ML models with these legacy environments can be technically complex and slow. APIs, middleware, and data transformation layers often have to be built before the first model goes live.

Talent needs

In addition to this, fintech projects require access to specialized talent, including not only data scientists but also ML engineers to productionize models and compliance specialists to ensure that every algorithm meets legal standards. These people can be in short supply and expensive. Without the right mix of skills, ML projects stall or never leave the lab.

Machine learning in fintech is powerful, but it’s not a plug-and-play solution. Success requires striking a balance between innovation and responsibility, encompassing protecting customer data, clearly explaining decisions, making informed investments, meeting regulatory requirements, and overcoming legacy challenges. The firms that get it right will not only reduce risk and costs but also build lasting trust with customers and regulators alike.

The most sustainable strategy is to modernize gradually, layering new ML components onto existing systems and upskilling internal teams along the way, bridging the talent and technology gap without disrupting core operations.

Conclusion

Machine learning is the foundation for tomorrow’s growth. The companies that embrace it now will be the ones shaping the industry’s next chapter, not scrambling to catch up.

With 25+ AI solutions delivered and over 3 years of hands-on work with LLMs, predictive analytics, and computer vision, Uptech has helped clients across fintech, healthcare, and other industries turn AI from concept into real business impact.

For example, the medical document processing system we worked on automated data extraction from lab forms and physician notes, reducing manual review time by around 30–34% and ensuring full HIPAA compliance.

Our approach combines strategic discovery, data security (GDPR, HIPAA, AI Act compliance), and fast proof-of-concept delivery — often within just two months.

Ready to future-proof your fintech business with machine learning? Contact us for a free consultation.